Executive Summary

and Introduction

Executive Summary

Georgia’s economy is growing, but prosperity remains out of reach for many families. In Forsyth County, just north of Atlanta, the median household net worth exceeds $720,000. In nearby rural Chattahoochee County, it’s closer to $15,000.1

These vast disparities—by geography, race, and wealth—are not anomalies; they are the result of generations of unequal access to asset-building opportunities. For families without wealth, even a small financial emergency can derail progress toward homeownership, education, or small business formation. As a result, Georgia’s persistent wealth divide continues to constrain economic mobility and limit the state’s full potential.

These wealth disparities don’t just reflect the past – they shape the future, limiting the ability of children born into low-wealth households to move up the economic ladder. Georgia — like much of the Southeast — has among the lowest rates of intergenerational economic mobility in the United States2. In most parts of Georgia, a child born to parents in the bottom 20 percent of the income distribution has less than a five percent chance of rising to the middle class, reflecting persistent and intergenerational cycles of poverty.3

This report makes the economic case for children’s trust accounts, or baby bonds, as a state policy to address Georgia’s growing wealth inequality4. Baby bonds – publicly funded trust accounts for children would provide Georgia newborns vulnerable to poverty with a safety net for their future, giving young adults capital needed to go to college, help purchase a home, start a business, or reinvest into Georgia’s economy in other meaningful ways. By design, baby bonds would invest more in children from lower-wealth families, helping to close the wealth divide while benefiting all communities across Georgia.5

Key Findings

- A universal baby bonds program in Georgia could build $1.4 billion in new wealth per birth cohort.6

- Eligible children could access up to $16,000 by age 18 under the proposed model.

- Rural counties—especially in South and Central Georgia—would benefit most due to higher rates of low-wealth births.

- Baby bonds would advance economic mobility, reduce future public assistance needs, and help close Georgia’s racial wealth divide.

Recommendation

Georgia should implement a baby bonds program with universal eligibility and tiered contributions, as proposed in House Bill 2847 and House Resolution 998 (2025). Under this model, eligible newborns would receive a starter deposit and children in lower-wealth families (e.g. those on Medicaid) would receive substantially larger deposits or annual top-ups. By age 18, eligible youth could accumulate up to $16,000 in a trust account, depending on investment growth.

This report assesses the state of wealth in Georgia currently, evaluates the cost and impact of several funding scenarios – from a basic universal plan to a more generous targeted plan – and finds that the progressive model would deliver the greatest reduction in Georgia’s wealth divide while remaining financially feasible and making an investment that would yield high returns in the form of a more prosperous generation of Georgians.

Introduction

Wealth—traditionally defined as the assets a family owns minus their debts—is a bedrock of financial security and opportunity.9 Yet wealth is distributed very unevenly in Georgia, leading to stark differences in life outcomes.10 While income allows families to get by month-to-month, wealth provides the resilience and springboard for families to get ahead.

A nest egg can finance a down payment on a home, seed a business venture, or put a young adult through college – investments that build prosperity across generations. Unfortunately, many Georgia families have been historically excluded from wealth-building, whether due to low incomes, lack of inheritance, or discriminatory policies11. As a result, our state today grapples with deep wealth and income inequality along racial and geographic lines.12 Addressing this inequality isn’t just a moral imperative – it is essential for Georgia’s long-term economic health.

Georgia’s context highlights why a bold policy like baby bonds is worth considering. The state’s population of 10.7 million is diverse and growing. Atlanta’s booming metro area fosters substantial wealth creation, yet many rural communities have abundant strengths that remain underinvested, limiting their asset-building opportunities. Nearly 15 percent of Georgians live in poverty (and poverty rates in some rural counties exceed 30 percent).13 Moreover, Georgia ranks 37th in the nation for child well-being, partly due to high rates of child poverty and limited family assets. 14

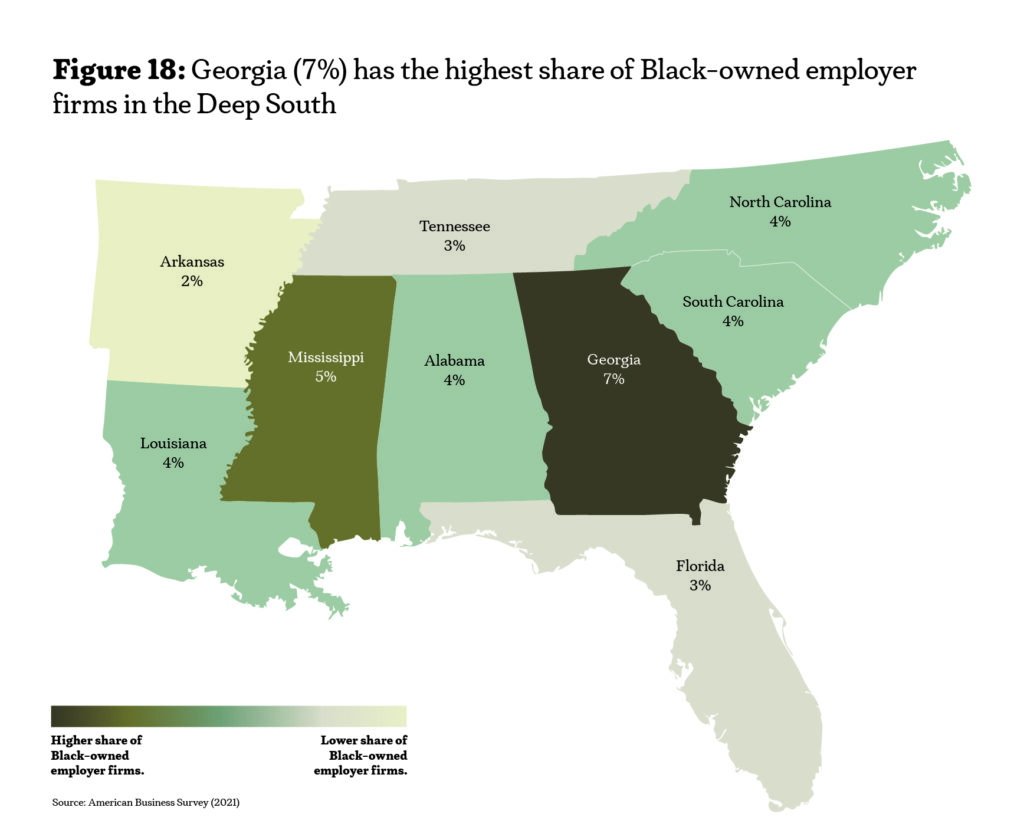

Crucially, wealth inequality in Georgia falls along historic racial lines.¹⁵ Generations of Black families were prevented from accumulating assets – first through slavery and sharecropping, penal colonies, later via Jim Crow segregation, redlining in housing, and exclusion from financial markets.15 These public policies created a yawning racial wealth divide that persists today: Georgia’s typical White family has about $180,949 in wealth versus just $21,733 for the typical Black family.16

At the same time, wealth inequality in Georgia is not solely an urban or racial issue – it has a clear geographic dimension. Three in four of Georgia’s 159 counties are rural, and many have not shared equally in the state’s economic growth. Approximately 17 percent of the state’s wealth is held in rural counties despite the vast majority of the state being rural, while 83 percent of the wealth is in non-rural counties. For example, in affluent Forsyth County north of Atlanta, the median net worth is over $720,000, while in rural Chattahoochee County it’s around $15,000.17

Such extreme differences reflect the concentration of high-paying jobs and real estate values in metro areas versus the chronic underinvestment in rural South Georgia. The result is a patchwork economy: some Georgia families enjoy stability and plenty, while many others whether in Atlanta’s Southside or Appalachia’s hill country — have little or no wealth to fall back on. Since policy choices created many of these disparities,18 smart and bold policy choices can help reduce them.

Faced with these challenges, state leaders have begun exploring solutions to boost household wealth and reduce inequalities. Traditional approaches have included spurring job creation, improving education, and offering tax credits for working families. While important, these measures alone haven’t closed the wealth divide, in part because they do not directly provide assets to those starting with very little or none.

This is where baby bonds enter the discussion. Baby bonds propose to endow every child with a small trust fund at birth, which the child can claim upon reaching adulthood for wealth-building uses.19 By giving children — especially those from low-wealth families — a lump sum of capital as young adults, baby bonds aim to break the cycle of intergenerational poverty. In recent years, policymakers in Georgia have taken note: legislation was introduced in 2025 to create a Georgia Baby Bonds program.20 These developments signal growing recognition that wealth building – not just income support must be part of Georgia’s policy toolkit to foster shared prosperity.

“Baby bonds propose to endow every child with a small trust fund at birth, which the child can claim upon reaching adulthood for wealth-building uses.”