Policy Pathways:

Building Black Wealth Through Structural Change

Bridging the racial wealth divide in the South will require ambitious, multi-faceted action. The good news is that research and practice offer a menu of proven and promising solutions. These range from direct financial interventions (like baby bonds and down payment assistance) to institutional reforms (like strengthening fair lending enforcement and supporting cooperative ownership models). All these approaches share a common principle: targeting the underlying structures that create and sustain wealth inequality, rather than placing the onus on individuals alone. We recommend a comprehensive strategy centered on community wealth-building, with public policies designed in partnership with Black communities themselves.

Key Pillars of a Black Wealth-Building Agenda for the South

1. Invest in Babies and Youth (Closing the Inheritance Divide): One of the boldest ideas gaining traction is a federal or state-level “Baby Bonds” program. Under baby bond proposals, every child would receive a trust account at birth (with larger deposits for lower-wealth families) that grows over time and can be used in young adulthood for wealth-building purposes (e.g. buying a home, starting a business). Analysis by the Center for American Progress found that a nationwide baby bonds policy, combined with other supports, could shrink the White–Black average wealth ratio from 6:1 today to roughly 1.9:1 by 2060.60 That is a profound improvement. Legislation for baby bonds has been introduced in Congress and in some states across the South, like Georgia, Louisiana, and North Carolina. Given the South’s racial wealth gulf, Southern states should pilot their own baby bond programs or supplement federal ones if enacted. Early estimates suggest a universal baby bond program could provide each Black child from a low-wealth family with $25,000–$30,000 by age 18 – enough for a college tuition or seed capital for a first home. This would directly counteract the lack of inherited wealth that impedes so many Black young adults in the South.

In addition, expanding Children’s Savings Accounts (CSAs) and college savings programs can foster asset-building habits and help families accumulate some wealth for education. Southern states can look to places like Maine that have implemented CSAs for every newborn.61 While typically smaller in scale than baby bonds, CSAs (especially with progressive matching for lower-income families) can narrow the savings divide for Black children. Education-specific funds, paired with scholarships and student debt forgiveness, will reduce the crushing debt loads Black students carry. We strongly support targeted student debt cancellation and greater Pell Grants to enable Black graduates to start their post-college without negative net worth.

2. Boost Black Homeownership and Housing Security: Given housing’s outsized role in wealth, aggressive steps are needed to increase Black homeownership in the South and ensure Black homeowners can build equity on par with others. Policymakers should:

- Provide Down Payment Assistance and First-Generation Homebuyer Programs: States should create special funds to assist first-time homebuyers who are first-generation homeowners (a disproportionate share of whom are Black or Brown). Research shows that lack of down payment is the top barrier for otherwise qualified Black renters to buy homes.

Enforce Fair Lending and Tackle Bias in Mortgage Underwriting: State banking regulators and attorneys general should actively test for discrimination at banks and mortgage companies. The extremely high denial rates for Black applicants documented earlier are not fully explained by credit profiles. Strengthening enforcement of the Equal Credit Opportunity Act and Fair Housing Act is critical. In practice, this means more funding for fair housing organizations to do audit testing, stiff penalties for lenders with unexplained racial disparities, and pushing for inclusion of alternative credit data (like rent and utility payments) to improve Black credit scores. Emerging technology like algorithmic underwriting must also be monitored to ensure it doesn’t perpetuate past bias.

Address Appraisal Bias: States can require training and diversified hiring for home appraisers and encourage the use of standards that value homes based on property characteristics, not neighborhood racial makeup. The federal Property Appraisal and Valuation Equity (PAVE) task force has issued guidance on this. Southern cities should pilot review panels for appraisals in communities with large populations of people of color and penalize appraisers who consistently undervalue Black-owned homes.

Expand Affordable Housing and Limit Predatory Practices: Inclusionary zoning (requiring new developments to include affordable units) and community land trusts can help more Black families attain stable housing and eventually ownership. Local governments should also crack down on contract-for-deed and rent-to-own scams that have proliferated in the South’s Black communities (these often charge excessive prices and keep deed title until fully paid, with high risk of loss). Preserving existing Black homeownership is as important as creating new owners—this means foreclosure prevention programs, heir property legal assistance (to help families clear titles and keep ancestral land), and property tax relief for long-term low-income owners facing rising taxes due to gentrification.

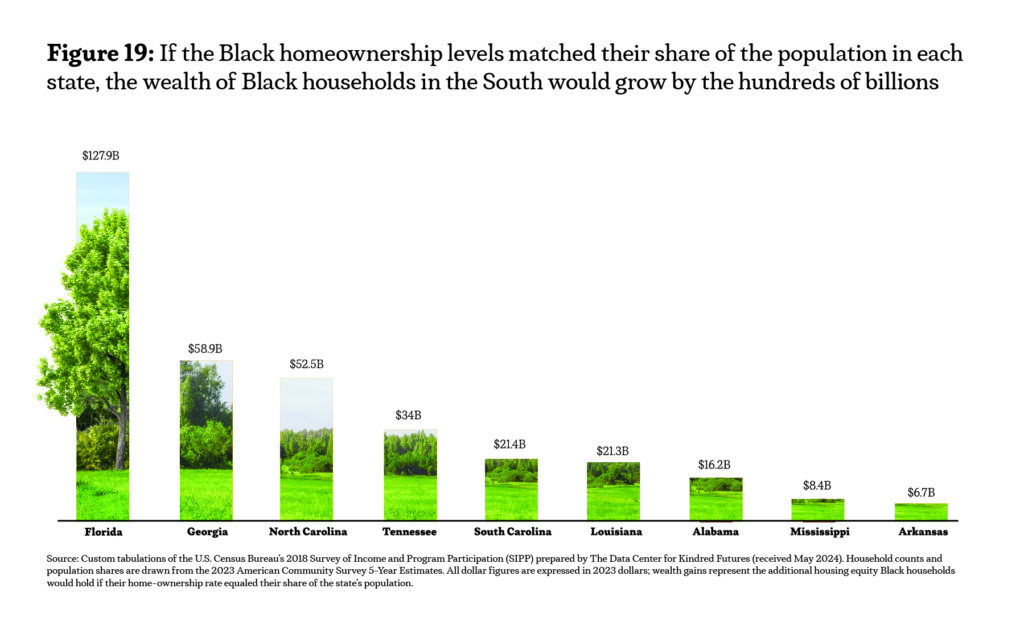

If these measures are implemented, we could see Black homeownership in the South rise significantly over the next decade – potentially closing the homeownership rate divide by several points. In addition, more equitable home values would increase Black wealth directly. Our analysis indicates that if Black homeownership rates were aligned with their population share, there would be a significant infusion of housing wealth into Black communities. Using state-level data on total owner-occupied units, current Black homeownership figures, and median Black home values, we determined the target number of Black homeowners that would reflect their demographic presence. For example, in Alabama, the divide suggests that an additional 108,250 Black households could become homeowners, potentially adding around $16.24 billion in housing wealth. In Florida, closing this divide could contribute an estimated $127.85 billion in additional housing wealth.

3. Strengthen Financial Infrastructure and Inclusion: Financial inclusion is about ensuring everyone has access to the tools for saving and borrowing at fair terms. To empower Black households in this regard, we recommend:

- Support CDFIs, MDIs, and Credit Unions: Community Development Financial Institutions (CDFIs) and Minority Depository Institutions (MDIs) (like Black-owned banks) have missions to serve underbanked communities. Southern states should partner with them by depositing some state funds in MDIs, offering loan loss reserves to encourage more small-dollar loans, and funding CDFI-led credit builder programs.

- Crack Down on Predatory Lending: State legislatures can enact or tighten interest rate caps on payday and title loans (e.g. capping APR at 36% as many states do for military personnel). They can also strengthen regulation of installment lenders and rent-to-own retailers. While some argue these services fill a need, the evidence is clear that they trap borrowers in cycles of debt. Expanding access to small-dollar loans via CDFIs or postal banking could replace predatory lenders with safer options. For medical debt, states should increase charity care requirements for hospitals and support Medicaid expansion (where not adopted) to reduce the burden of unpaid medical bills fueling debt problems.

- Implement Supportive Tax Policies: States should adopt and expand family-supporting tax credit initiatives—including refundable Earned Income Tax Credits (EITCs), child tax credits, and child care tax credits—to provide direct financial support to low- and middle-income families. By ensuring these tax credits are refundable, states can guarantee that families with little or no tax liability still receive a meaningful benefit. Such measures would increase disposable income, promote savings, and reduce financial stress, thereby empowering families to invest in education, health, and housing—key drivers of long-term wealth accumulation. Enhanced tax credits also serve to counteract structural inequities, as they provide targeted support to communities historically excluded from traditional wealth-building opportunities.

4. Increase Black Incomes and Labor Protections: Income from work may not guarantee wealth, but it’s a necessary foundation. Policies to raise Black incomes and eliminate earnings disparities include:

Raise the Minimum Wage: Several Southern states still use the federal minimum wage ($7.25). Raising it (e.g. to $15 or more gradually) would disproportionately benefit Black workers, who are often in the lowest-paid jobs. Estimates show a $15 minimum would increase Black workers’ earnings by billions and reduce poverty rates significantly in the South.6

- Strengthen Worker Protections and Unions: Strengthening collective bargaining and worker centers in the South can be a powerful tool for closing the wealth divide. Data from the Federal Reserve’s Survey of Consumer Finances show that the median wealth for a union household is roughly 1.7 times that of a nonunion household, with the biggest percentage boosts going to workers of color and those without a college degree. By securing higher wages, retirement plans, and job stability through collective bargaining, unions help ensure that more families—especially in historically under-resourced communities—build meaningful wealth. States should expand legal protections for organizing, invest in worker centers that educate and advocate for employees, and incentivize employers to bargain responsibly. Efforts such as repealing or reforming “right to work” laws, strengthening labor law enforcement, and supporting multi-employer bargaining models can give Southern workers a true voice in negotiations.63

- Invest in Job Training and Pipelines to High-Paying Fields: To address the underrepresentation of Black workers in STEM, finance, and management, states should invest in targeted, no-cost training from high school through mid-career. For example, incentivizing apprenticeships in the trades and advanced manufacturing for Black youth, and partnering with HBCUs on internship pipelines to Fortune 500 companies in the South. The aim is to move more Black workers into careers that offer retirement plans, stock options, and growth potential – crucial ingredients for wealth accumulation.

- Support Returning Citizens: The South has a high rate of incarceration which has removed many Black men (and women) from the workforce. Re-entry policies that address training, job placement, and seals/restricts records for formerly incarcerated people can help them secure employment, thus contributing to family incomes and stability.

If Black median incomes rise (closing the racial income divide which currently is around 60–70 cents on the dollar), it will have a multiplier effect on wealth over time. More income means more ability to invest in homes, businesses, and education for the next generation.

5. Facilitate Black Business Growth and Asset Ownership: To expand Black entrepreneurship and asset ownership (beyond just housing), we propose:

- Dedicated Funds for Black Entrepreneurs: States should seed Black business loan funds (or incubators) that provide capital and technical assistance. For example, a Deep South Entrepreneur Fund could pool public, philanthropic, and private dollars to offer low-interest loans to Black-owned startups and expanding firms, administered by CDFIs or MDIs. Similarly, expanding state small business credit initiatives to focus on minority business enterprises can leverage federal dollars to catalyze local lending.

- Support Cooperative and Community Ownership: Community wealth-building emphasizes collective ownership models as well. Southern cities can encourage development of Black-led worker cooperatives (where workers share profits and equity) and community land trusts (which keep land ownership local and affordable). For instance, Jackson, MS and Atlanta, GA have nascent cooperative movements that could be bolstered through technical support and start-up grants. These models ensure that wealth generated remains anchored in the community. Cities could also expand community ownership of housing (via land trusts or limited equity co-ops) in historically Black neighborhoods to prevent displacement and allow residents to gain equity as a group.

- Reclaiming Black Land and Agriculture: Given the massive Black land loss documented, efforts to restore and retain land ownership are key. This includes funding legal aid for heirs’ property resolution (to clear titles and avoid forced partition sales), fully implementing the USDA debt relief for farmers of color, and supporting young Black farmers to acquire land. Some nonprofits are facilitating land purchases back to Black farmers – state agriculture departments can partner in these. Retaining land ensures that value appreciates in Black hands rather than being lost. Over time, even modest acreage can be an asset base to leverage for loans or to rent out for income.

The combined effect of these business and asset initiatives would be to increase the share of wealth generated by the Black community that stays in the Black community. More successful Black businesses mean more Black millionaires, more local jobs, and more role models/mentors. It also diversifies the economy, making it more resilient and innovative by tapping talent that is currently under-utilized.

6. Embrace Reparative and Bold Public Policies

Incremental measures alone are unlikely to fully close a wealth divide centuries in the making. Thus, we call on Southern states and cities to consider reparative measures that directly transfer resources to build Black wealth. These could include:

- Reparations or Wealth Restoration Programs: Following the lead of cities like Evanston, IL (which instituted a housing reparation for Black residents using a marijuana tax), Southern jurisdictions can design reparations to address specific historical injustices. For example, a state might fund reparations for descendants of those who suffered under enslavement, Jim Crow voter suppression and land theft. While comprehensive reparations is a federal endeavor (H.R. 40 and related efforts are ongoing), states can take initiative in piloting programs.

- Universal Policies with Racial Equity Benefits: Many broad progressive policies would substantially help close racial divides. Examples include medical debt payoff, strengthening Social Security (Black seniors rely heavily on it, having fewer assets), and robust safety nets (child allowances, guaranteed income, etc.). A federal analysis by RAND found that a mix of wealth-building policies (including direct allocations to Black households) totaling about $1.6 trillion would eliminate the median wealth divide – a large sum, but not unimaginable in the context of government budgets (for comparison, the PPP pandemic program was nearly $800 billion). The economic boost from such investment would likely generate new tax revenue over time to offset costs.64

- Democracy and Power-Building: Lastly, none of these economic policies will be enacted without the political power of Black communities. Protecting voting rights and ending practices that dilute Black votes (gerrymandering, voter suppression) is fundamental. Political capital translates into public investment decisions. States that empower Black voters (like through strong community engagement in budgeting) see more equitable outcomes. Building a movement for Black wealth also means reframing the narrative – as Kindred Futures emphasizes, Black wealth means freedom, and advancing it moves us closer to the beloved community.

Conclusion

The challenge of building Black wealth in the South may seem daunting, but it is also achievable with vision and commitment.

This report has shown that the racial wealth divide is not a result of personal failings or cultural deficiencies; rather, it is the product of deliberate policy choices and systemic biases that have favored one group while disadvantaging another. Therefore, it will take intentional policy interventions to dismantle these barriers and cultivate the roots of Black wealth.

The South cannot reach its full potential while a significant portion of its people are constrained by an unjust wealth divide.

By unearthing Black prosperity, we mean digging into and removing the deep obstacles—much like removing rocks and hardpan soil to let a tree grow deep roots. The policies recommended here form a blueprint for that process. They align with best practices of just economic development: targeted universalism (universal programs designed to lift up the historically marginalized), reparative justice, public investment in human capital, and fostering ownership and agency in communities.

Breaking the wealth-building barriers will require bold action, but the benefits will reverberate across society. When a Black family can purchase a home in a good neighborhood without unfair hurdles, the neighborhood benefits. When a Black entrepreneur can access capital to start a business, she creates jobs and innovation that boost the local economy. When Black children grow up with savings and without crushing debt, they become adults who can spend, invest, and contribute to growth.

The South cannot reach its full potential while a significant portion of its people are constrained by an unjust wealth divide. The time to act is now—before another generation is lost to the compounding effects of inequality. The year 2025 finds us at a crossroads: we can continue on the current path and watch median Black wealth head toward zero, or we can choose the path of shared prosperity and freedom.

The roots of wealth in the South run deep; they have been nourished for some and starved for others. It is time to till the soil, to fertilize the dreams of those who have been denied, and to grow an inclusive prosperity that honors the contributions of Black Americans. In doing so, the South will move closer to the beloved community where, indeed, all can share in the wealth of the earth—fulfilling Dr. King’s vision and securing a brighter future for generations to come.