Structural Barriers to Black

Wealth-Building Today

Building Black wealth in the South requires navigating a minefield of structural obstacles. These barriers are interrelated and mutually reinforcing. For example, lower incomes make it harder to save for homeownership, which means missing out on home equity gains, which in turn limits capital for entrepreneurship or education for the next generation. In this section we examine several key structural factors—geography, housing, debt, education, employment, and enterprise—illustrating how each contributes to the racial wealth divide. Throughout, the focus remains on community-level structures rather than individual behavior, consistent with a community wealth building perspective.24

Geography and Community Infrastructure

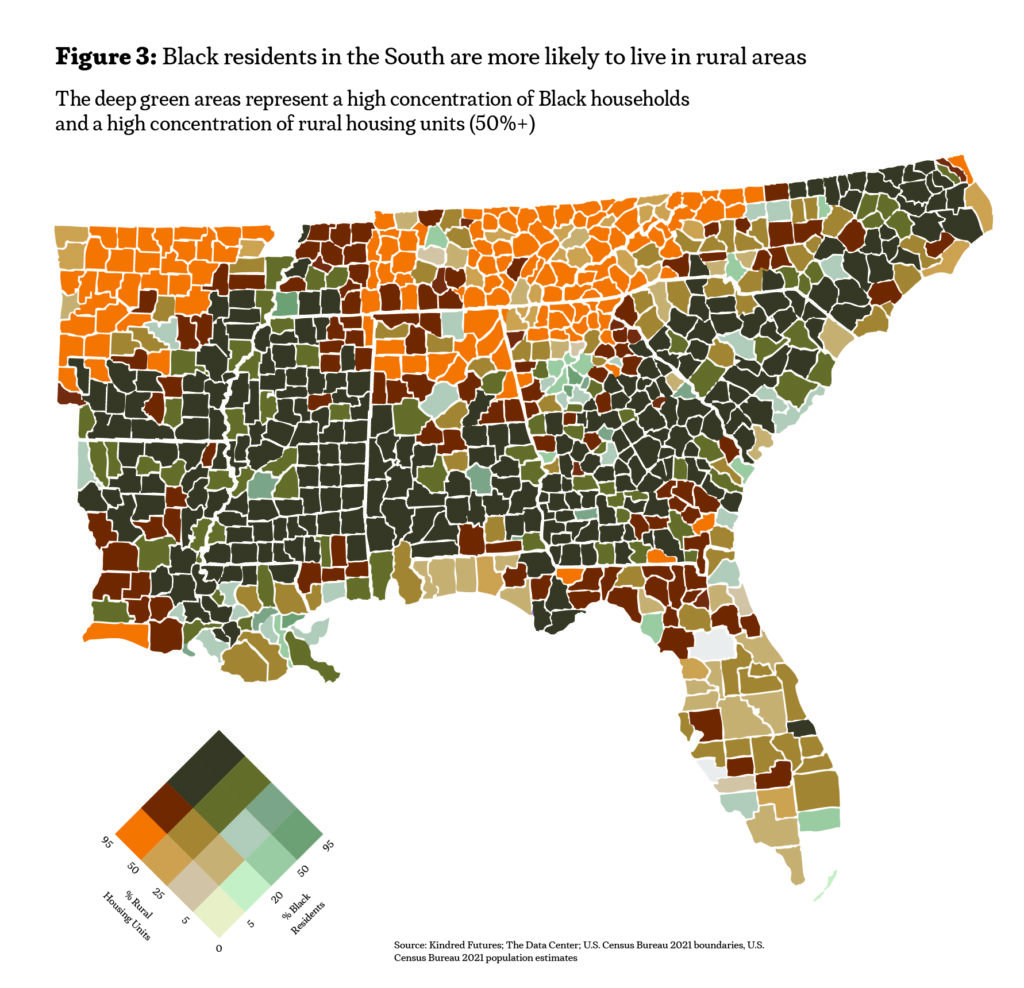

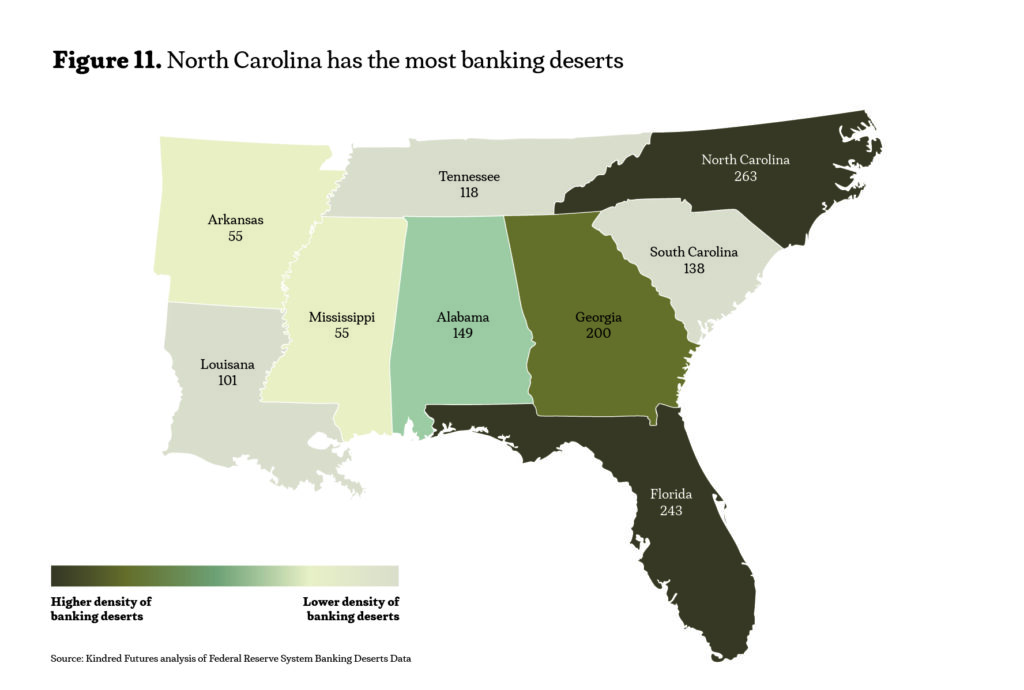

A significant share of Black Southerners live in rural, high-poverty counties—especially in the historic Black Belt stretching from eastern North Carolina through Louisiana and Arkansas. These counties, often majority-Black since Reconstruction, suffer from chronic disinvestment.25 People who live in these counties have limited access to banks, businesses, and broadband that drive wealth in metropolitan areas.26

The map highlights counties (green-shaded areas) that are both predominantly Black and predominantly rural (50% or more rural households). These are concentrated in the Deep South, reflecting how Black residents are more likely to live in rural areas than the national average. In states like Mississippi, Alabama, and Louisiana, entire swaths of Black communities are rural and isolated from economic growth centers.27

Rural Black communities face a double bind of racial and geographic disadvantage. Limited tax bases and exclusionary policy decisions have left many without adequate roads, internet, hospitals, or schools. For example, residents of Alabama’s Black Belt must often drive hours to reach a bank or accredited medical facility.28 Such divides impose extra costs (time, travel, high fees for alternative financial services) that inhibit saving and investment. Fewer employers operate in these areas, contributing to lower home values and out-migration of youth.29

Yet not all urban areas guarantee prosperity either. While cities like Atlanta and Charlotte offer more jobs, Black residents in those cities still contend with segregation, higher costs of living, and discrimination in labor and housing markets.30

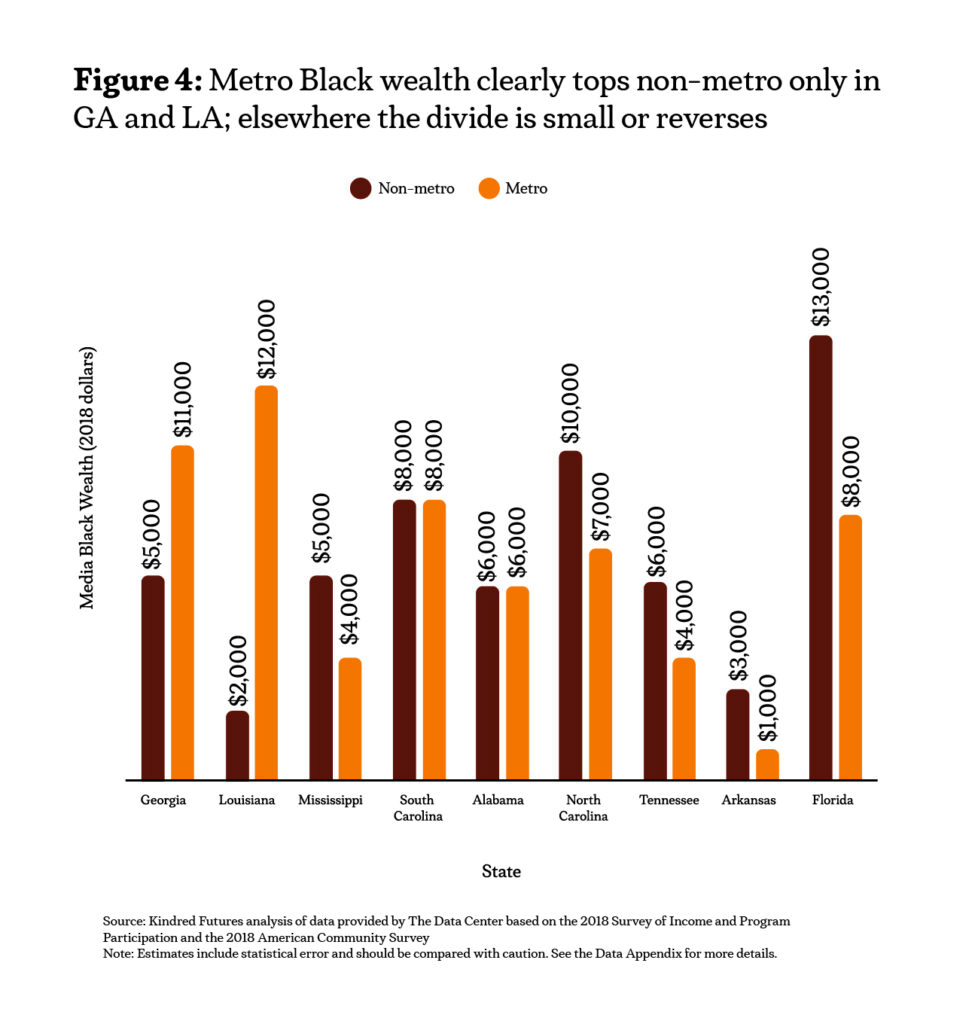

Across much of the Deep South, rural Black households hold wealth on par with— and in several cases modestly above—their metro-area peers. In Florida, for example, the median Black household in non-metro counties reports about $13,000 in wealth versus roughly $7,000 in metro areas; smaller rural gains also appear in Arkansas, North Carolina, Mississippi and Tennessee. These differences may reflect assets such as inherited land, lower living costs, or reduced exposure to gentrification and other urban pressures. Still, most state-level divides are only a few thousand dollars, so additional data are needed to confirm whether the pattern is real or within survey error (see Appendix).

By contrast, White households enjoy a clear metro advantage in every state: in Mississippi, for instance, median White wealth reaches $101,000 in metro areas versus $81,000 in rural counties. The comparison underscores that geography alone does not close racial wealth divides—urban growth continues to translate into larger gains for White residents, while structural barriers limit the returns available to Black families.

Place-based solutions are critical. Investing in rural Black communities (e.g. through targeted federal funds for infrastructure, broadband, and healthcare) can improve the foundation for wealth creation where it’s needed most. At the same time, urban policy must address the fact that

Black residents in cities aren’t automatically sharing in prosperity.

Black Asset Portfolios In The South

Almost everywhere in the Deep South, owning a home is the main way Black families build wealth. In most states a house makes up about a third to half of everything a household owns. But what sits on top of that base changes from place to place. In Mississippi and Arkansas—where good jobs and banks are hard to find—wealth is packed into things you can see and touch: houses, land, and even cars. In Georgia, helped by the economic pull of Atlanta, families have a wider mix: more savings in retirement plans, more money in small businesses, and a bit more in other financial accounts. North Carolina and Tennessee fall somewhere in between.

Relying so heavily on a single item—a house—creates risks. If local home prices slide, a Black family can lose a big slice of its wealth overnight. At the same time, having little money in retirement accounts or small businesses means missing out on other ways to grow wealth over time.

Fixing this calls for practical help. Grants that cover first-time down payments or urgent home repairs can keep housing wealth safe while bringing more people into ownership. Easier, low-cost loans can help Black entrepreneurs grow their companies and spread their bets beyond the family home. And simple, automatic retirement plans at work can help more people set aside money for the long haul. Taken together, these steps would give Black families a sturdier, more balanced path to building and keeping wealth.

Homeownership and Housing Equity

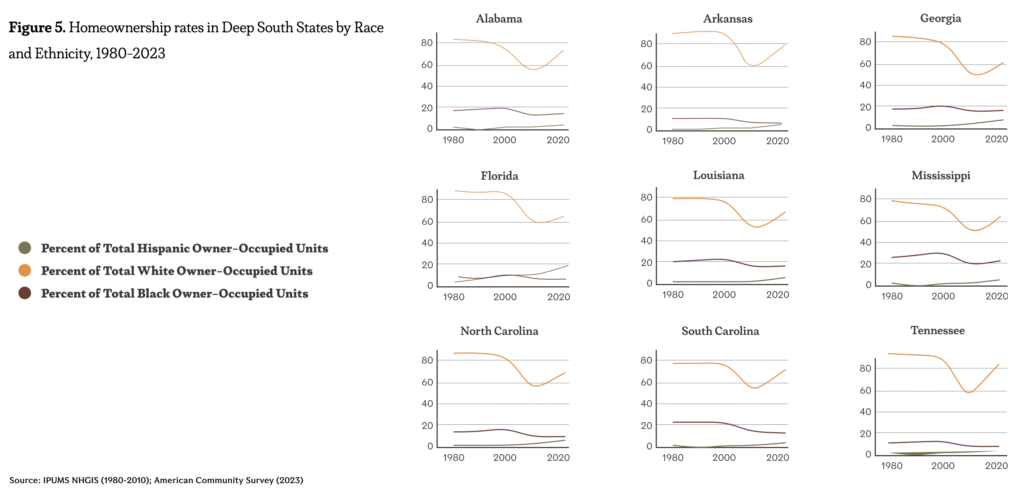

Owning a home has long been the cornerstone of the American wealth-building model – yet for Black Southerners, housing wealth has been elusive. The homeownership divide between White and Black families remains as wide as it was 50 years ago in many Southern states. Several factors contribute to this for Black families: lower incomes and savings for down payments, discriminatory lending (past and present), and residential segregation that has suppressed Black home values.31

Today, White households still make up the large majority of homeowners in every Deep South state. Even in Mississippi – the state with the highest proportion of Black residents – Black families represent only 21% of owner-occupied homes (down from 27% in 2000). States like Georgia and Florida saw a dip in Black homeownership share after the 2008 housing crash, and only slight rebounds since.32

None of these states have regained the Black homeownership levels seen in the 1990s. This matters because homeownership is strongly correlated with wealth: nationally, the median homeowner has 40 times the wealth of the median renter.33 In the South, where property values tend to be lower than coastal states, home equity still dominates household assets (often 50% or more of total wealth for middle-class families).

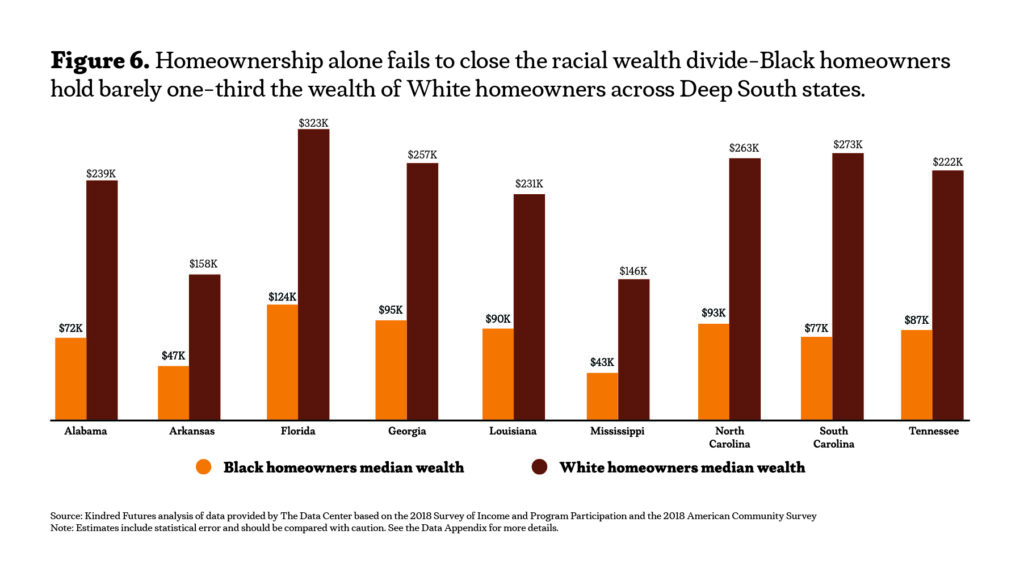

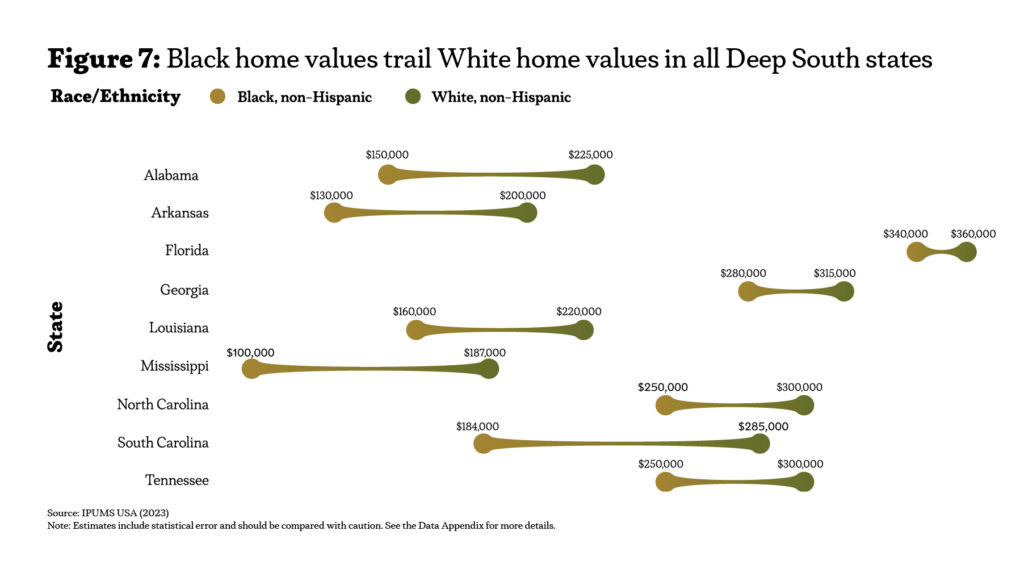

Even among homeowners, substantial wealth disparities persist between White and Black households in the Deep South. Each bar pair represents the median wealth of White versus Black homeowners in a given state, and in every case, White homeowners hold more wealth—often two to three times as much. For instance, while Black homeowners in Georgia report one of the highest median wealth levels in the region (about $95,000), it still lags well behind the $257,000 median for White homeowners. The pattern underscores a core finding of this report: homeownership alone does not eliminate the racial wealth divide, indicating that deeper structural factors—such as appraisal bias, historical exclusion from credit, and ongoing discrimination—continue to shape financial outcomes for Black households across the South.

Even when Black families do own homes, those homes are typically worth less on the market than White-owned homes, due to decades of segregation and disinvestment in Black neighborhoods. Our analysis found that across Deep South states, the median value of homes owned by Black households is tens of thousands of dollars lower than the median value of White-owned homes in the same state. In South Carolina, for example, the median Black-owned home is worth about $101,000 less than the median White-owned home. Florida shows the smallest divide (around $20,000, perhaps because many Black homeowners in Florida are in higher-cost markets like Miami), but most states have divides of $50,000 or more. Lower home value means less equity to borrow against for education or business, and less wealth to pass to heirs.

Major drivers of these disparities include:

- Historic Redlining: 20th-century policies restricted Black buyers to certain areas, often of lower initial value, with limited financing available.34 Those maps of inequality persist today, as homes in formerly redlined (majority-Black) neighborhoods are appraised significantly lower than similar homes in White neighborhoods.

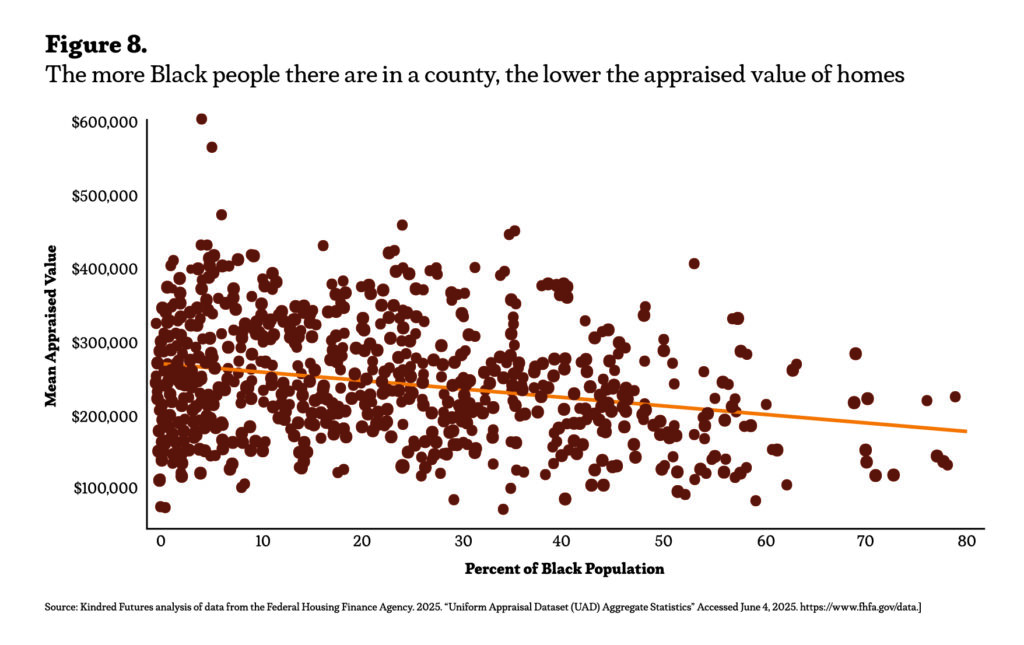

- Appraisal Bias: Even today, studies show homes in Black neighborhoods are undervalued by 20-23% relative to their features, simply because of racial composition.35 The chart below illustrates a clear negative correlation between a county’s share of Black residents and its average appraised home value: as the percentage of Black population increases, the mean appraised value of homes tends to decrease. Biased appraisals and lower comps mean Black sellers get less and Black owners accumulate equity more slowly.

- Differential Access to Home Improvements: With less wealth and credit, Black owners may struggle to invest in home repairs or upgrades that increase value. Additionally, cities often invest less in infrastructure (parks, schools, transit) in Black and rural neighborhoods, affecting property values.

Mortgage Denials and Financing

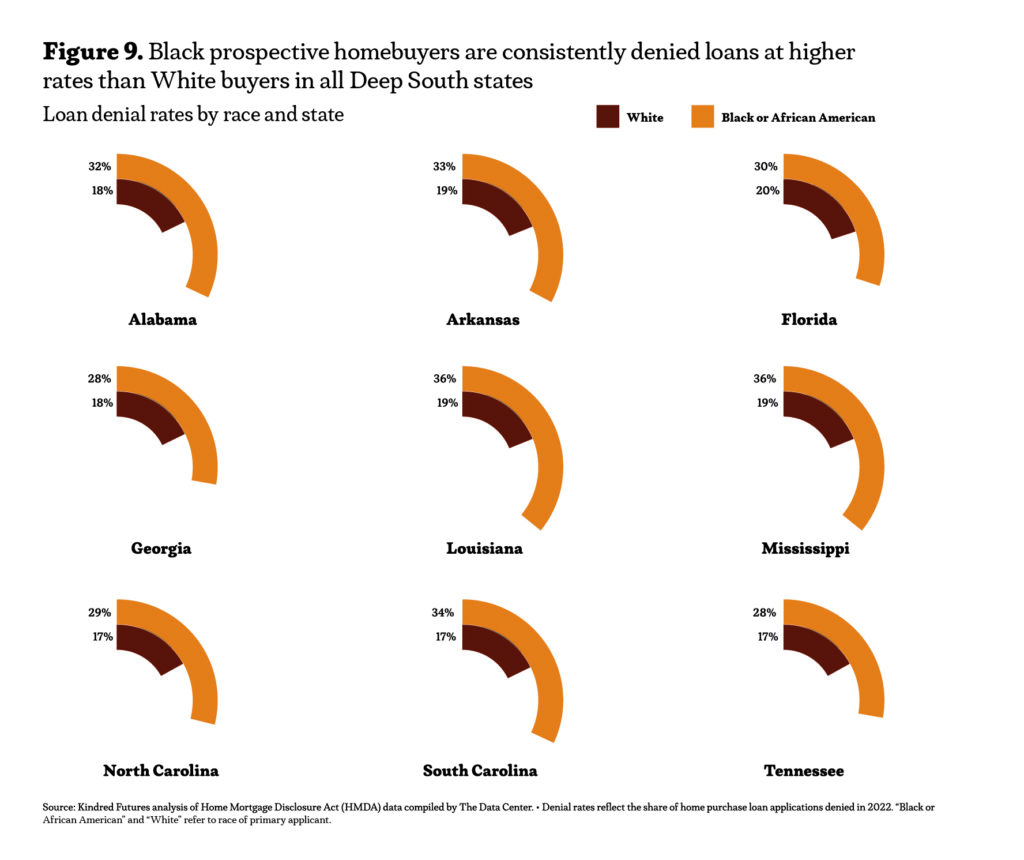

Perhaps the most glaring current barrier is the racial divide in mortgage lending. In every Deep South state, Black applicants are denied home loans at far higher rates than White applicants of similar income. Black denial rates range from 28%–36%, versus 10%–20% for White applicants. These numbers reflect factors like lower average credit scores for Black households, higher debt-to-income ratios, and ongoing discrimination by lenders.36 The result is fewer Black buyers and a continuation of segregated housing patterns. Even those who qualify may face higher interest rates or less favorable terms, meaning they build equity more slowly and pay more over time.

Because of these housing dynamics, Black families in the South miss out on the primary source of wealth-building. Lower homeownership not only means less wealth today, but less intergenerational wealth tomorrow (since homes are a common inheritance or financial safety net). The racial disparities in housing also reinforce other inequities: neighborhoods with low homeownership and wealth tend to have under-resourced schools, fewer businesses, and lower tax revenue, perpetuating a cycle of disinvestment.37 The stability and credit advantages of homeownership (e.g. fixed housing costs, ability to borrow against equity) remain out of reach for many Black Southerners, keeping them more vulnerable to eviction, displacement, and wealth-draining rent payments.

Debt, Credit and Financial Inclusion

Debt Overhang

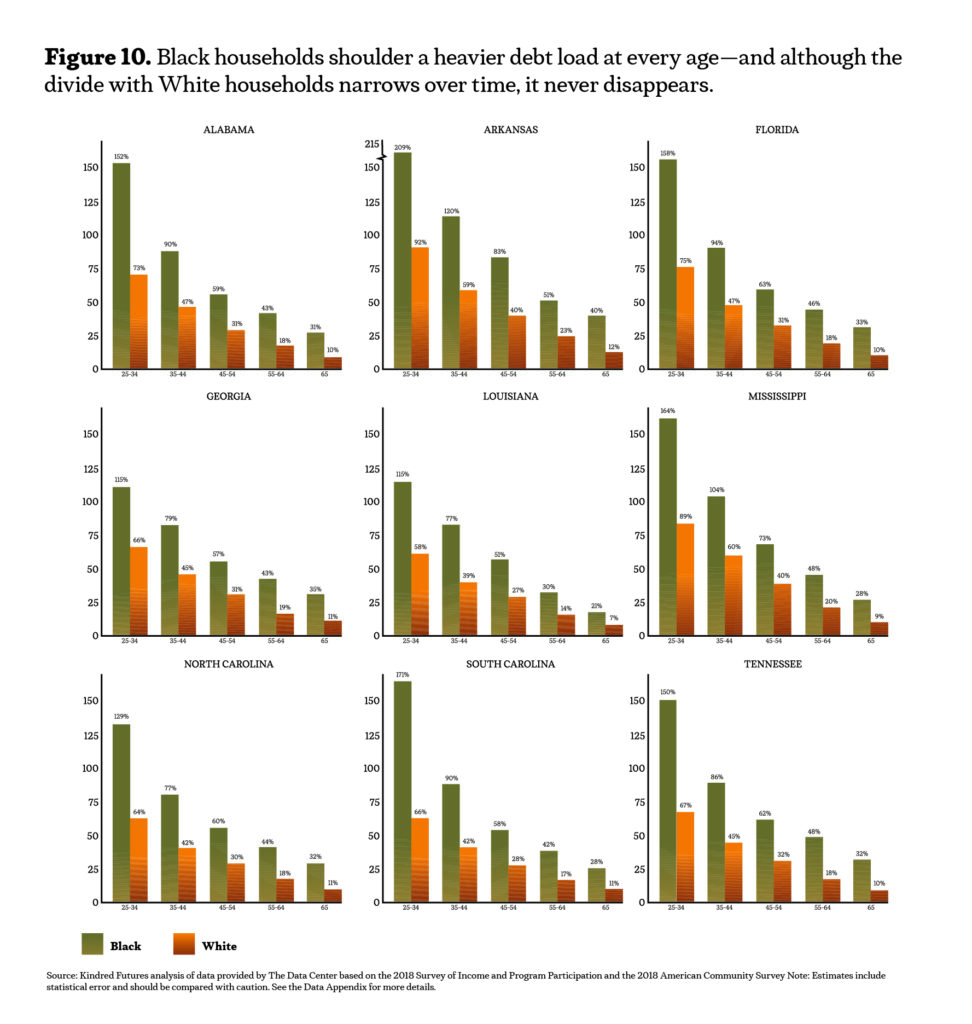

Many Black households in the South begin their financial lives not with assets, but with debts that outstrip those assets. This was vividly shown in a multi-state study of debt-to-asset ratios: across all age groups, Black families carry significantly higher debt relative to what they own than White families do. In young adulthood (ages 25–34), the typical Southern Black household has debts equal to 150% or more of their assets (meaning their net worth is negative) in states like Florida and Alabama. By comparison, young White households had debt around 60%–80% of assets on average.38

Several structural issues drive these debt disparities:

- Lower Inherited Wealth: With scant inheritances or family wealth to draw on, Black students often must borrow more for college. Black college graduates average tens of thousands more in student loans than White graduates. This burden delays home-buying and business investment.39

- Credit Constraints and Predatory Lending: Black communities historically lacked fair access to mainstream credit (due to redlining and lower bank presence). This void was filled by predatory lenders offering high-interest loans (payday lenders, subprime mortgages, auto loans).40 These debts accumulate rapidly. In Black neighborhoods of the South, it’s not uncommon to see clusters of check-cashers and payday loan shops where banks are scarce.41 The result: Black borrowers face higher interest costs and fees, making payoff harder.

- Income Volatility and Emergency Expenses: Black families, on average, earn less and have less savings, so when emergencies strike (medical bills, car repairs), they must resort to credit. Medical debt is a huge issue in states that did not expand Medicaid (many in the South).42 Uninsured or underinsured Black households often incur medical debts that go unpaid, damaging credit scores and leading to collections

- Financial Exclusion: About 10%-15% of Black households in several Deep South states have no bank account. Lacking access to basic, low-cost financial services forces reliance on expensive alternatives. For example, without a bank, one might use pawn loans or rent-to-own stores with exorbitant rates, falling deeper into debt. High unbanked rates in places like Mississippi and Louisiana correlate with high levels of delinquent debt.

High Delinquency and Credit Damage

A significant share of Black Southerners live in rural, high-poverty counties—especially in the historic Black Belt stretching from eastern North Carolina through Alabama and Mississippi. These counties, often majority-Black since Reconstruction, suffer from chronic disinvestment. People who live in these counties have limited access to banks, businesses, and broadband that drive wealth in metropolitan areas.

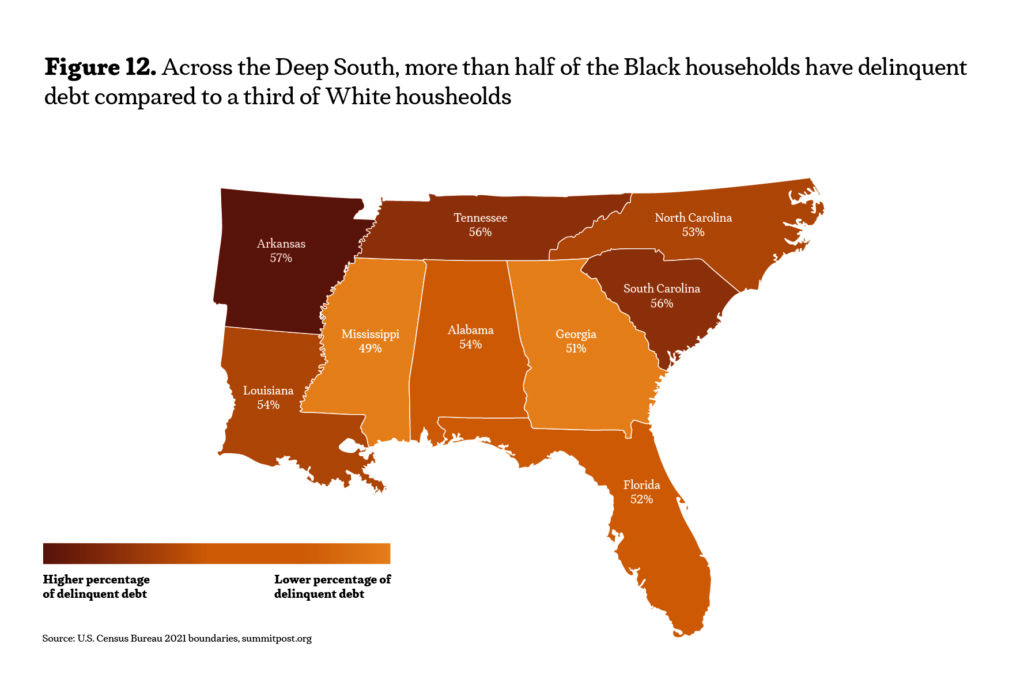

Consequently, Black Southerners are far more likely to have delinquent debt (debt past due or in collections). In every Deep South state, over half of Black households have some delinquent debt on their credit record, compared to roughly one-third of White households. This includes items like unpaid medical bills, defaulted loans, or past-due credit card balances. Figure 12 showcases the uniformity of Black debt delinquency across southern states, which ranges from 50 to 57 percent.

Across the Deep South, more than half of Black households has debt in collection or past due, whereas roughly a third of White households do. This debt overhang impedes wealth-building, as families with damaged credit pay higher interest and struggle to get mortgages or small business loans.

Why does this matter for wealth? High debt and poor credit scores create a vicious cycle. Credit score divides mirror wealth divides: median credit scores for Black adults in Southern states are typically 50–80 points lower than for White adults. For instance, the median Black credit score in Georgia is 628 vs. 710 for Whites. A low score makes it harder to qualify for affordable loans, forcing reliance on subprime lenders and perpetuating high debt costs. It can even affect employment and housing, as many employers and landlords check credit. Thus, addressing the debt burden is central to closing the wealth divide: if Black families must spend a large share of income servicing debt, they cannot save or invest for the future. Additionally, money spent on interest payments to predatory lenders represents wealth flowing out of the community (often into the coffers of distant corporations).

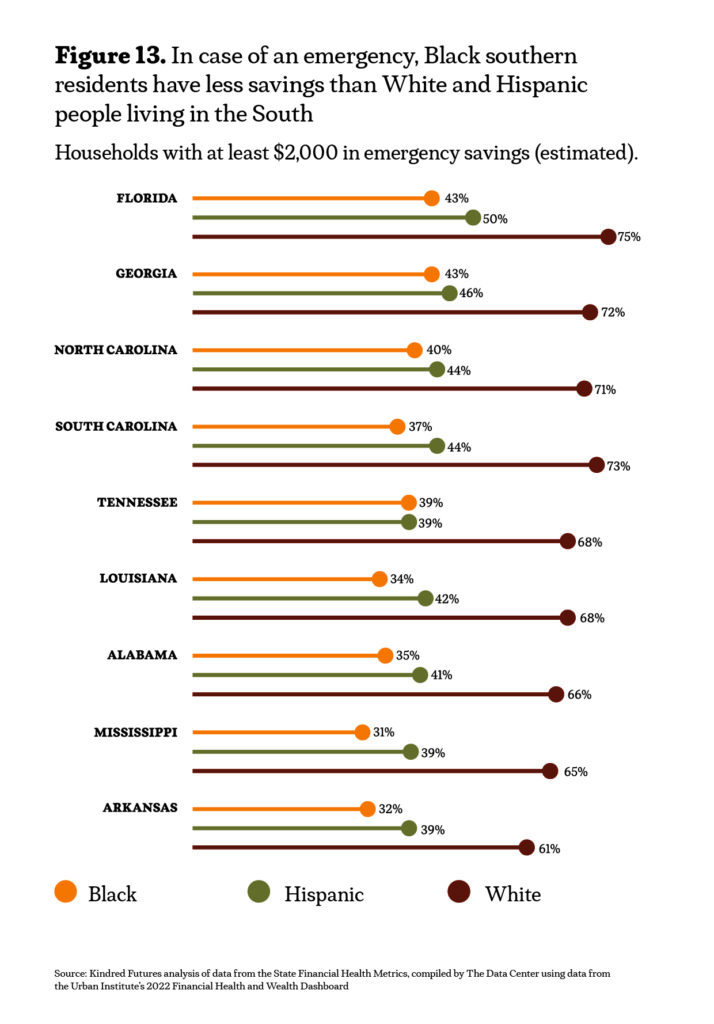

Emergency Savings and Financial Resilience

One indicator of this challenge is the lack of emergency savings. Surveys estimate that fewer Black residents have even a $2,000 rainy-day fund. Figure 13 shows that in every Deep South state, the percentage of Black households with at least $2,000 in savings is far below the percentage of White households. In Mississippi and Arkansas, only about 1 in 3 Black households have $2,000 set aside, versus about 2 in 3 White households. This means Black families are more exposed to financial shocks, which often leads to taking on expensive debt.

Improving financial inclusion—connecting Black communities to safe, affordable banking and credit—is a necessary step toward wealth equity. It involves expanding CDFIs and credit unions, regulating payday lenders, and initiatives like Bank On that encourage low-fee accounts. Without such measures, high debt will continue siphoning off Black income and preventing its conversion into wealth.

Racial Climate Resilience Divide

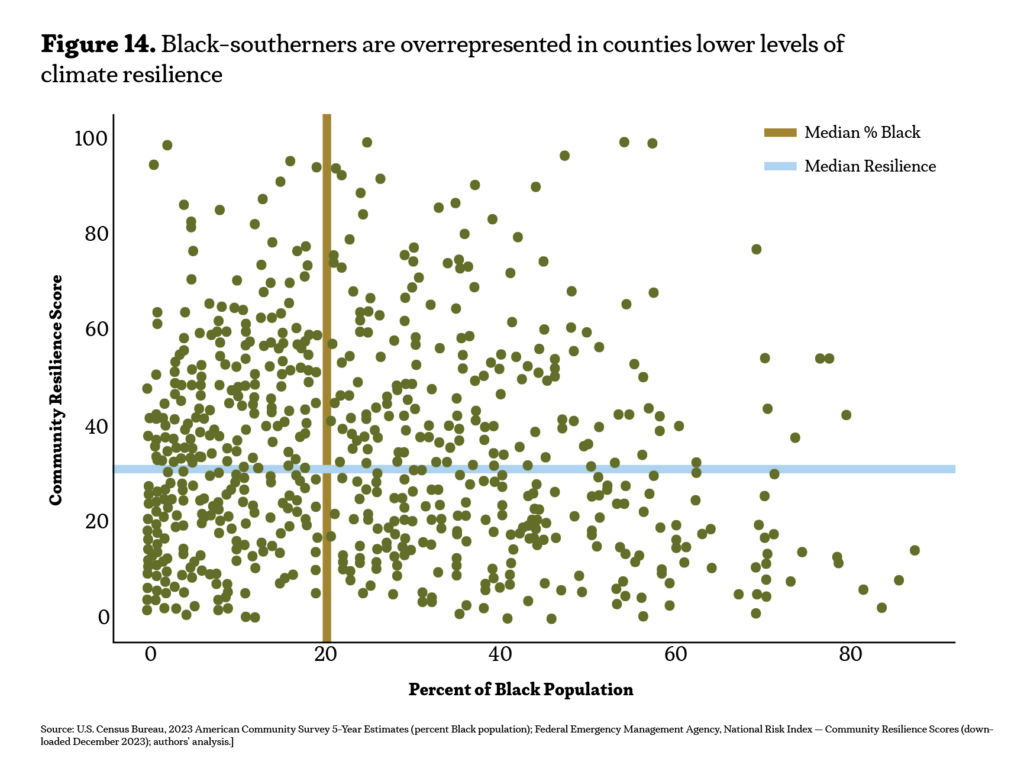

To deepen our understanding of how racial demographics intersect with climate disaster resilience in the Deep South, we conducted a quadrant analysis using county-level data from FEMA’s National Risk Index.43 The analysis compared each county’s percentage of Black population with its Community Resilience Score, a metric ranging from 0-100 that captures a community’s capacity to prepare for, respond to, and recover from climate disasters. By dividing the data along median values for both variables, we created four distinct quadrants that allow for a clearer picture of where disparities lie.

What emerges from Figure 14 is a striking pattern. The largest group of counties fall into the quadrant characterized by both high percentages of Black residents and low resilience scores. A smaller subset of counties stands out as outliers—those with both high Black populations and high resilience—but these are relatively rare.44 This suggests that while it is possible to build resilience in Black-majority communities, it is not the norm under current conditions.

The implications of this finding for Black wealth in the South are profound. Community resilience is more than a measure of disaster preparedness; it is a reflection of a community’s broader economic and institutional health. In counties where resilience is low, climate disasters like hurricanes are more likely to erode household wealth through property loss, job disruption, or displacement. For Black households in particular—many of whom already face barriers to asset accumulation—this creates a cycle of vulnerability that is hard to escape.45 Even moderate disasters can have outsized effects in these communities, especially when there are limited financial institutions, weak governance structures, and few opportunities for reinvestment.46

Moreover, resilience is closely tied to access: access to credit, to insurance, to reliable infrastructure, and to timely emergency response. In low-resilience, high-Black counties, these forms of access are frequently limited or unevenly distributed. This means that recovery takes longer, costs more, and is more likely to result in long-term displacement or disconnection from community wealth-building assets such as homeownership, local businesses, or inherited property.47 Without targeted investment, these patterns will continue to suppress economic mobility for Black families, perpetuating the racial wealth divide across generations.

Education, Employment, and the Racial Wealth Paradox

Education and employment are traditionally seen as routes to economic success. Black Americans in the South have made significant gains in educational attainment and professional employment over recent decades. However, the wealth divide in the region persists even for those who attain higher education or stable employment, due to structural inequities in the returns on those achievements.

Higher Education – Unequal Returns

College degrees substantially increase earning potential and wealth for Black individuals, but not as much as they do for Whites graduates. In fact, a median Black household headed by a college graduate still has less wealth than a median White household headed by someone with no degree.

One reason is the student debt burden mentioned earlier. Black graduates often begin their careers deep in the red. Another is housing – even a high-income Black professional may face discrimination in home appraisals or mortgage rates, limiting the wealth they can build from real estate. Additionally, Black college grads are more likely to be first-generation wealthy, meaning they might need to assist extended family,48 whereas White grads more often receive inheritances or parental help with home purchases.

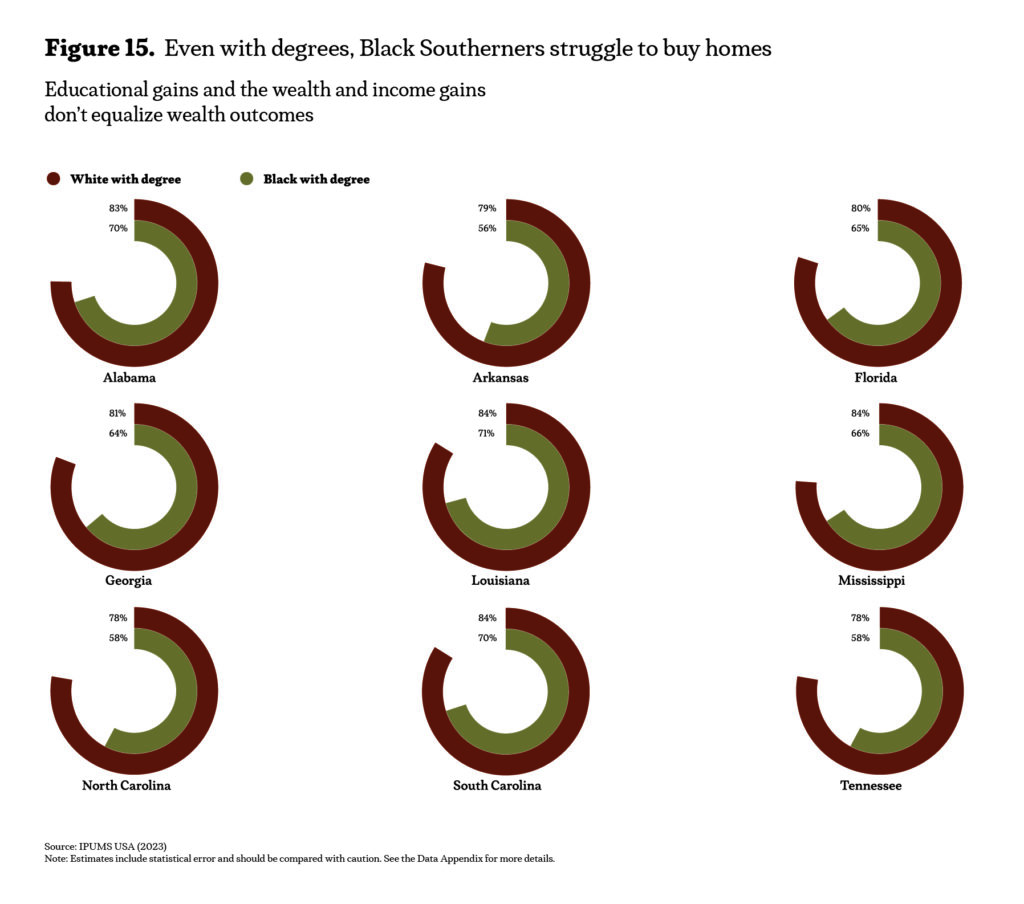

Figure 15 shows that even among households where the head has a college degree, White homeownership rates vastly exceed Black homeownership rates in each Southern state. For instance, in Arkansas, 79% of White college grads own homes vs. 56% of Black college grads.49 Lack of homeownership translates to a large wealth divide despite similar education. We see that education is not the “great equalizer” when structures like credit access and housing discrimination intervene.

Labor Market Segmentation

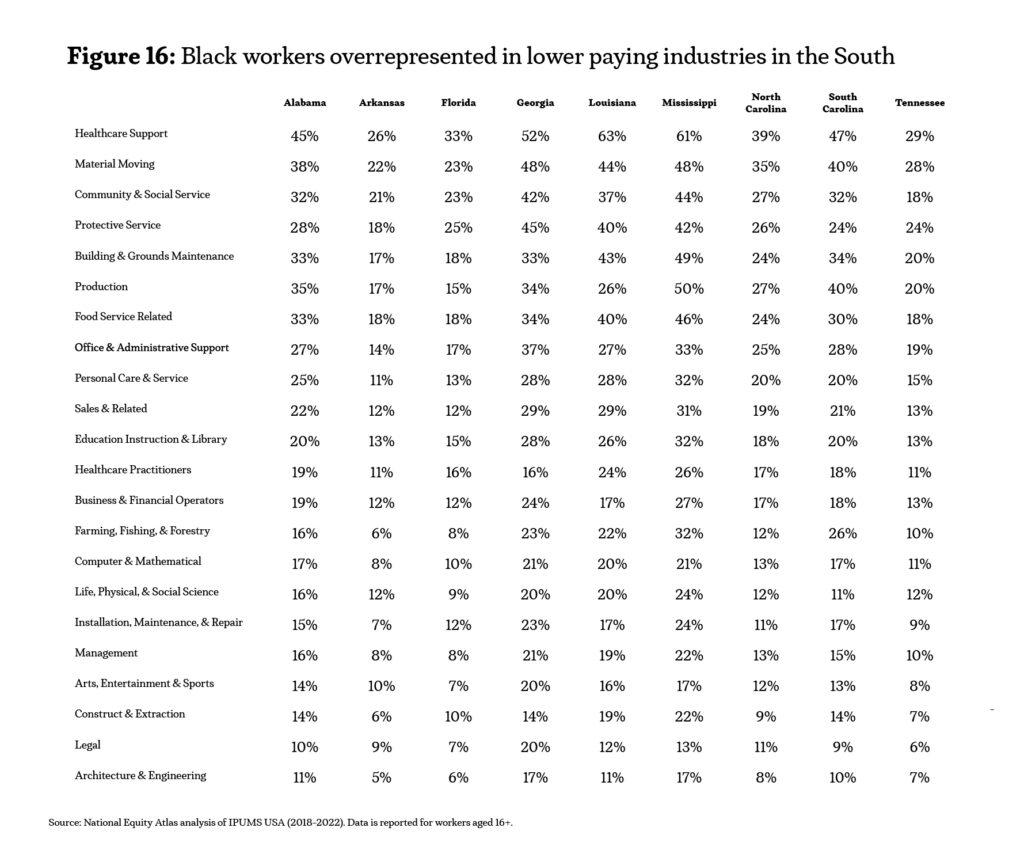

Black workers in the South are overrepresented in lower-wage occupations and underrepresented in higher-paying professions. This stems from both historical segregation in employment and ongoing bias in hiring and promotion. In healthcare, for example, Black employees are much more likely to be nursing aides or home health aides than physicians or pharmacists.

The figure below displays the percentage of each state’s workforce (in various sectors) that is Black. We see Black workers clustering in fields like Healthcare Support (e.g. nursing assistants), Transportation/Material Moving, Food Service, and Building & Grounds Maintenance – jobs that tend to have lower pay and benefits. In Louisiana and Mississippi, over 60% of healthcare support workers are Black, reflecting heavy reliance on Black women’s labor in caregiving roles.50 By contrast, in high-paying STEM or management roles, Black representation is often under 10% (e.g. only 10% of managers in Tennessee are Black).

Unequal occupational distribution means that even with similar education, Black workers often earn less. Pay divides persist within occupations too – research shows Black employees earn less than White employees in the same jobs, due to discrimination and weaker bargaining power.51 Lower earnings make it harder to save, leading to lower wealth.

Unemployment and Underemployment

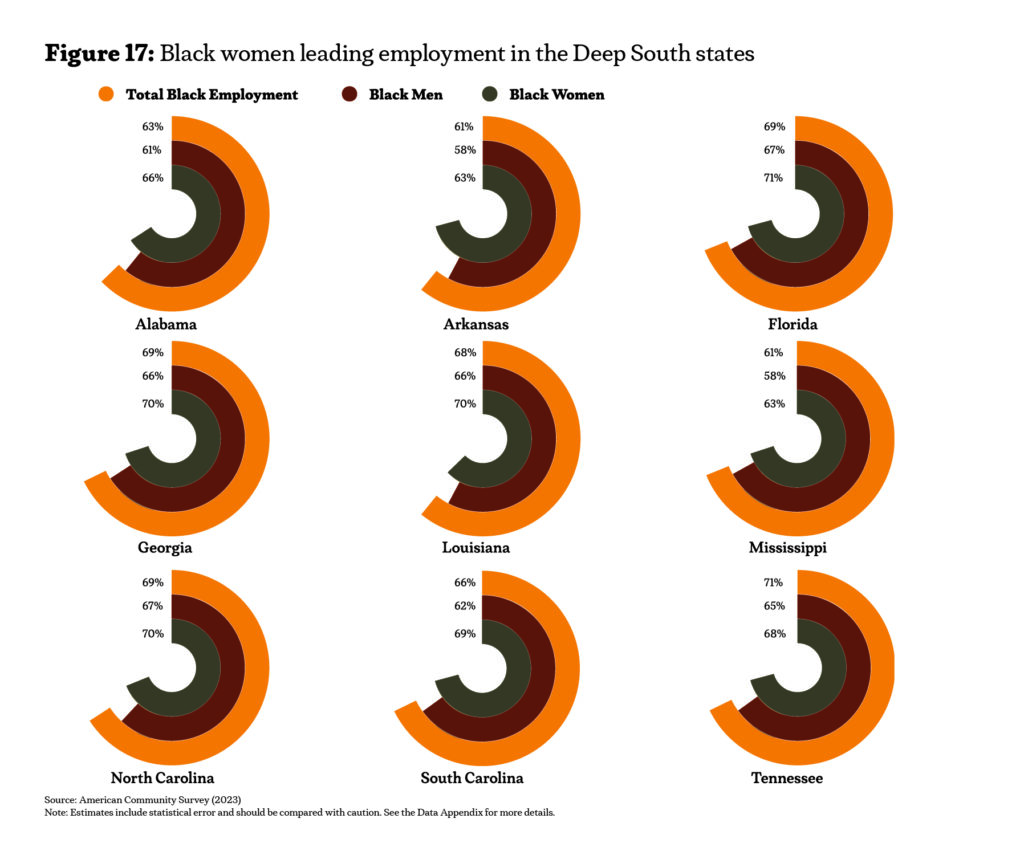

The Black unemployment rate has historically been about double the White rate, and the South is no exception. During economic downturns, Black workers are often first fired and last rehired.52 Moreover, many Black adults, especially men, have been sidelined from the labor force due to incarceration or health issues rooted in inequality.53 This has led to a phenomenon in some communities where Black women have higher employment rates than Black men.54 Indeed, data show that in every Deep South state, the employment-population ratio for Black women slightly exceeds that for Black men. In states like Florida and Georgia, 70% of Black women are employed compared to 67% of Black men. Black women’s strong work participation is commendable and often necessary for family survival, but because women’s jobs are often lower-paid (e.g. care work), this dynamic can still result in less wealth accumulation than in households with two high-earning spouses.

Education and hard work alone are not enough to build lasting Black wealth in the South when the rules of the game are rigged. We must rewrite the policies that shape access to opportunity. A more educated Black workforce cannot translate their credentials into wealth parity without changes in the systems around them: equal access to high-paying careers, fair compensation, protection from exploitation, and the ability to leverage income into assets (through homeownership, investments, etc.).

Entrepreneurship and Business Ownership

Entrepreneurship is often touted as a wealth-building path, yet Black business owners face steep uphill battles in the South. A healthy business ecosystem can create jobs and community wealth, but currently, Black-owned employer businesses (those with paid employees) are exceedingly rare in most Southern states. White business owners dominate the landscape, owning 70–82% of all employer firms in the region. By contrast, Black entrepreneurs own only 2–8% of employer firms, despite Black adults comprising 20–35% of the population in these states.55

The underrepresentation of Black businesses is not due to lack of ideas or talent; it stems from lack of capital and structural support:

Access to Capital

Starting or expanding a business requires seed money, collateral, or loans. Due to the wealth divide, the average Black entrepreneur has less personal/family wealth to draw on, and banks often hesitate to lend to those with limited collateral or lower credit scores. Black business owners in the South report difficulties obtaining loans from mainstream banks; many rely on personal savings or high-interest credit.56 Venture capital is even more skewed: nationally, less than 1% of VC funding goes to Black founders.57 This capital divide means Black firms often start smaller and grow slower. Because of historical exclusion, Black entrepreneurs may lack the networks that White entrepreneurs tap into for partnerships, clients, and mentorship. Southern states have a history of nurturing incubators and Chambers of Commerce for minority businesses (e.g. in Atlanta), but these resources need scaling across the region.

Historical Prejudices

For decades, Black-owned businesses were confined to serving Black customers in segregated markets, limiting their growth. Post-integration, many Black businesses struggled to compete with larger White-owned firms that had better financing. The closure of numerous Black banks and insurers in the late 20th century also constricted funding channels. The legacy is a smaller Black business sector overall.

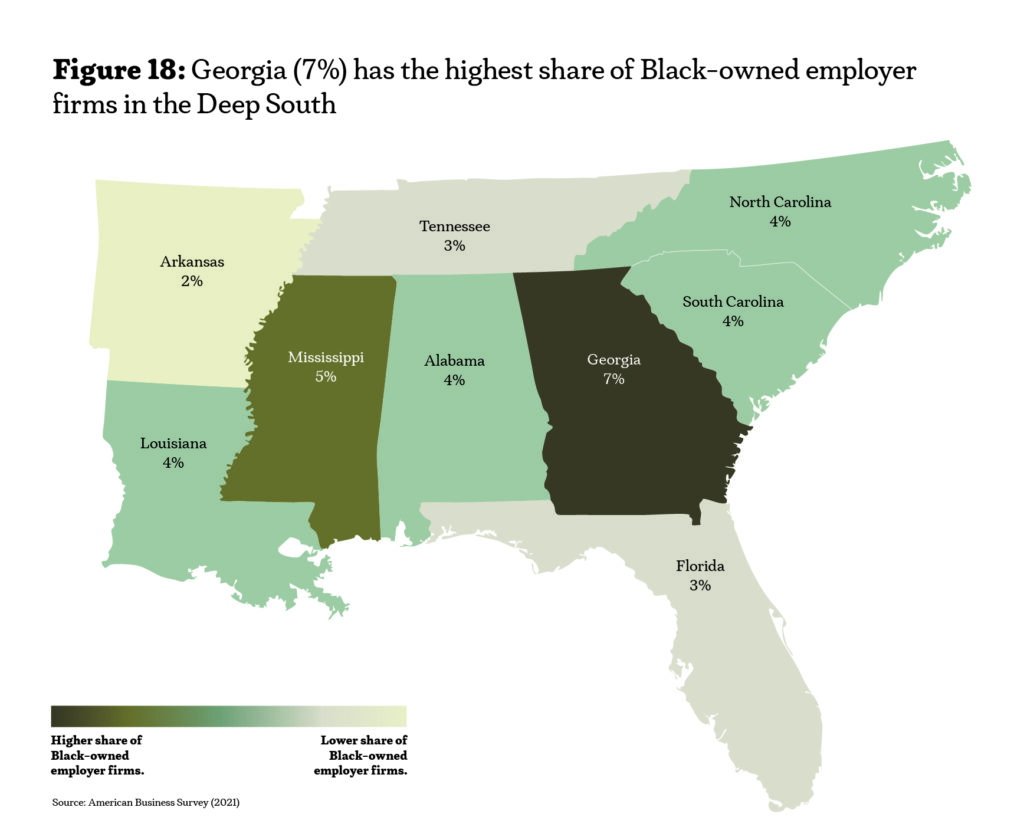

Georgia and Florida stand out as modest bright spots: Georgia has about 7% of firms Black-owned – likely influenced by Atlanta’s high concentration of Black entrepreneurs. Still, even in Georgia, Black residents are 32% of the population and only 7% of business owners. Mississippi has the lowest shares (5%), which is striking given Mississippi’s Black population size. This points to severe structural barriers in those states’ business environments.

The dearth of Black-owned businesses matters for wealth because entrepreneurship can yield substantial returns and create community jobs. When business ownership is so skewed, it reinforces the wealth divide: White owners accumulate profits and equity, while Black workers earn wages. Additionally, Black-owned firms are more likely to hire Black employees, so fewer Black businesses mean fewer employers who might proactively invest in Black communities.58

Summary: The Structural “Web” Underlying the Wealth Divide

The structural barriers outlined above do not operate in isolation – they compound. A hypothetical example illustrates this web of disadvantage: Imagine a Black college graduate in Alabama. She finishes school with significant student loans (debt), struggles to find a high-paying job in her field due to subtle hiring bias (employment barrier), ends up taking a job that doesn’t build wealth (occupational segregation), rents an apartment because she can’t afford a home down payment (housing barrier), accumulates little savings while servicing student debt (debt again), and can’t fall back on family wealth (historical divide). Even though she “did everything right” individually (got an education, worked hard), the structures around her limited each wealth-building step.

Having examined these barriers, the next section of this report turns to solutions. Encouragingly, evidence suggests that bold policies can produce major gains. For instance, new “baby bond” proposals would provide children with seed capital that, by adulthood, could substantially equalize wealth starting points. Reparative housing programs and debt forgiveness can free up Black income for saving rather than loan payments. The final section outlines a comprehensive policy framework – a kind of Marshall Plan for Black wealth – to address the intertwined factors we have discussed.