The Black Wealth Landscape:

Deep South States at a Glance

The Deep South is home to some of the largest Black populations in the United States—and some of the deepest racial wealth disparities.

This section compares key indicators of Black wealth across nine states: Alabama, Arkansas, Florida, Georgia, Louisiana, Mississippi, North Carolina, South Carolina, and Tennessee.

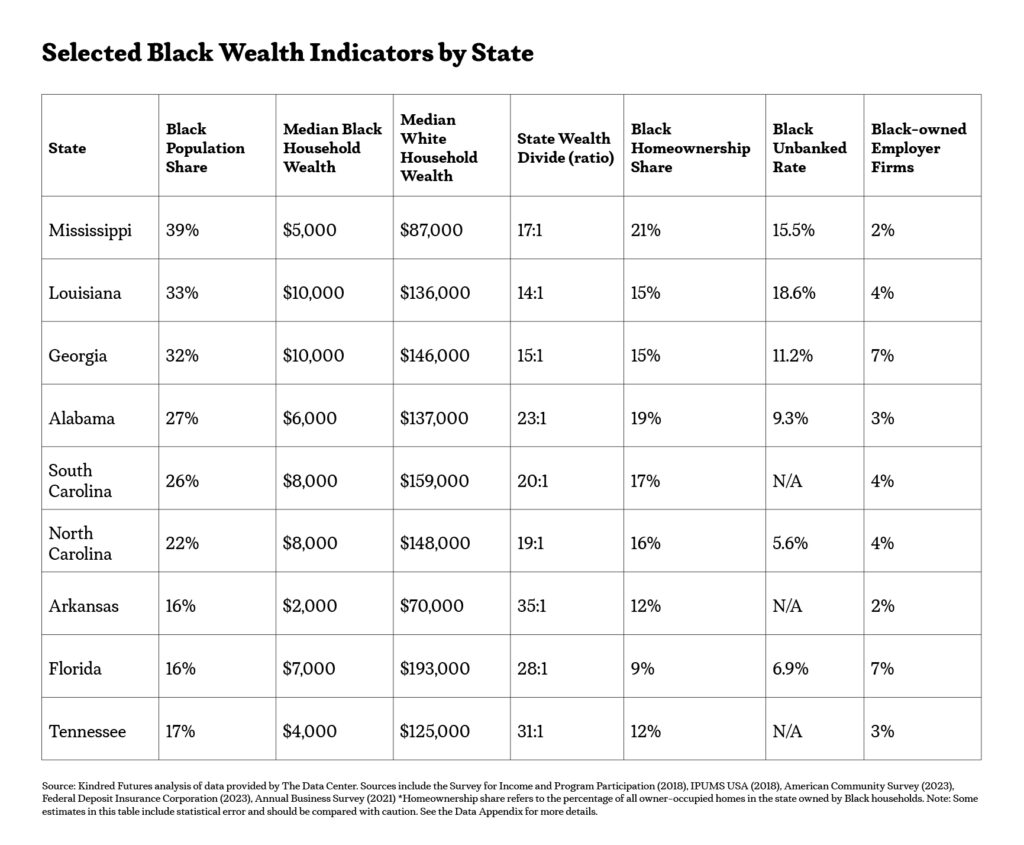

While each state has a unique history, the data reveals common challenges: low Black wealth, lagging homeownership, high debt and unbanked rates, and underrepresentation in business ownership. These are also important variations that can inform state-specific strategies. The table below provides a snapshot of the Black–White wealth divide by state, followed by highlights:

Mississippi:

The state with the largest Black population share (nearly 4 in 10 Mississippians) paradoxically has one of the South’s lowest median wealth figures for Black households ($5,000). White households in Mississippi hold roughly 17 times more wealth. Mississippi also has one of the highest rates of Black families lacking basic bank accounts (15.5% unbanked) and one of the highest Black home loan denial rates (36% denial). These indicators reflect deep, persistent exclusion despite the state’s large Black population.

Louisiana:

Louisiana is another Black plurality state (33% Black) where median Black wealth is extremely low ($10,000). Only about 1 in 5 homeowners in Louisiana are Black, down from nearly 25% in 1980 due to foreclosures and economic stagnation post-2008. Louisiana has one of the highest recorded Black unbanked rate in the South (18.6%). Black women’s labor participation in Louisiana is among the highest, reflecting their role as breadwinners (63% of Black women employed vs 56% of Black men).

Georgia:

Georgia boasts one of the region’s highest estimated median Black wealth figures (around $10,000) and the largest share of Black-owned businesses (7% of employer firms). These achievements owe much to Metro Atlanta’s robust Black professional class. However, the wealth divide remains vast—White median wealth in Georgia is about 15 times Black median wealth. Black Georgians also carry heavy student debt loads that eat into wealth gains. Roughly 29% of Black adults in Georgia hold a bachelor’s degree (highest in Deep South), yet education has not translated to proportional gains in wealth.

Florida:

Florida’s Black population (about 3.8 million people) has relatively high employment and entrepreneurship in some metro areas, but the typical Black household’s wealth is only about $7,000. Whereas White households in Florida hold 28 times more wealth (median $193,000. Florida’s Hispanic communities have attained higher business ownership (18% of firms) and homeownership than its Black communities, pointing to different structural barriers. Black Floridians also face one of the largest mortgage denial rates (30%).

Alabama & South Carolina:

Both states have Black populations around 25–27%, Black homeownership shares around 15–20%, and Black median wealth at approximately $6,000 and $8,000, respectively. Black Alabamians have made some progress in education (i.e. college attainment has improved), but wealth remains very low. For instance, Alabama’s Black middle class holds a fraction of White wealth at similar levels of education. South Carolina’s Black Belt regions remain plagued by high poverty, and the state has seen only modest recovery in Black homeownership post-recession.

North Carolina:

With booming finance/tech hubs, North Carolina has seen rising overall wealth, but its racial wealth divide persists. Black households have a median wealth of $8,000 (and many younger households have zero or negative net worth). Notably, North Carolina has the one of the lowest Black unbanked rates (5.6%), thanks in part to urban centers like Charlotte with better banking access. Still, only about 6% of NC businesses are

Black-owned.

Tennessee & Arkansas:

These states have the smallest Black population shares in the Deep South and some of the lowest Black wealth metrics. Tennessee’s median Black wealth ($4,000) is one of the lowest reported. However, Tennessee offers an interesting case where rural Black wealth (around $6,000) may slightly exceed urban Black wealth ($4,000), perhaps due to a few Black landowners or lower cost of living in rural areas. Arkansas similarly shows rural Black households may be doing marginally better than urban ($3,000 vs $1,000), but overall Black wealth is extremely low and Black business ownership is only 2%. This underscores the need for basic financial infrastructure and investment in Black communities that have been long neglected.

Overall, this snapshot paints a picture of entrenched disadvantage: Black communities across the South hold vastly less wealth and are underrepresented in key wealth-building domains (homeownership, business ownership) despite in many cases comprising a large portion of the population. This is not due to individual choices or deficits in financial literacy—it is the result of structural barriers. As the next section details, common factors such as limited access to capital, housing inequality, labor market segregation, and debt burdens continue to hold back Black wealth accumulation in all of these states. By understanding these structural issues, policymakers can design interventions that target the root causes rather than the symptoms.

Place-based solutions are critical. Investing in rural Black communities can improve the foundation for wealth creation where it’s needed most.