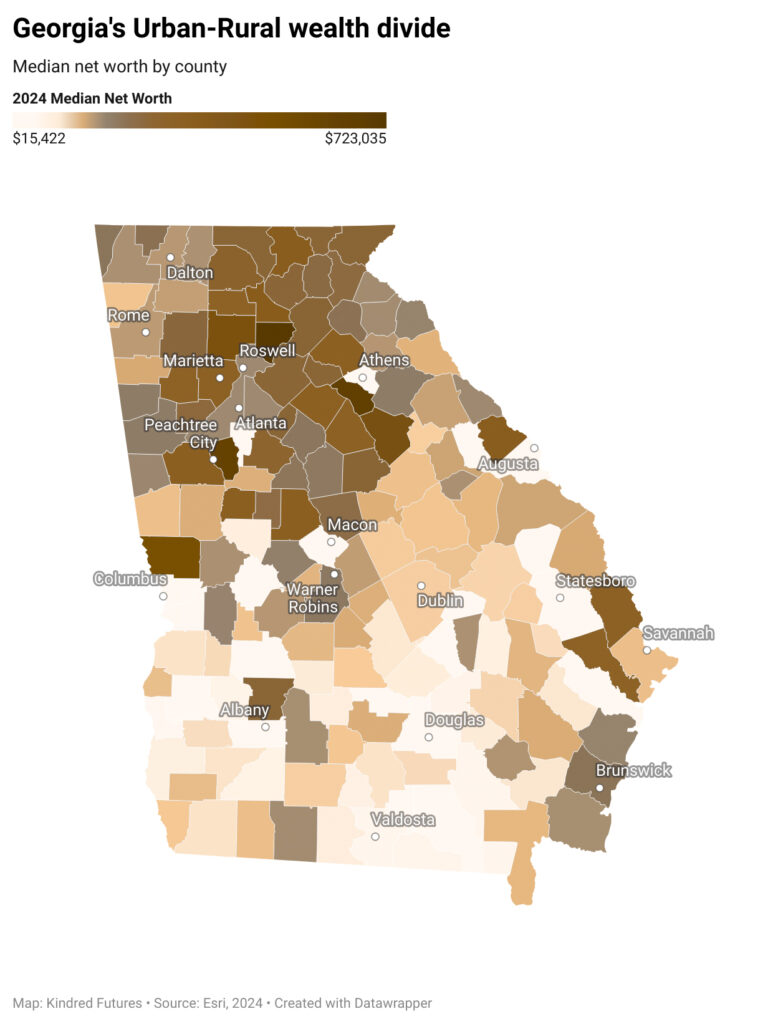

Georgia’s urban-rural wealth divide also deserves attention. Despite the vast majority of the state being rural, approximately 17 percent of the state’s household wealth is held in rural counties while 83 percent of the wealth is in non-rural counties.26 In North Georgia’s Forsyth, Cherokee, and Fayette counties (suburban areas near Atlanta), median household net worth exceeds $700,000. By contrast, many rural counties in east and South Georgia show median net worth figures below $100,000. For instance, in Chattahoochee County (south-western Georgia), the median household has around $15,000 in wealth.27

These differences reflect structural factors: rural economies often rely on a few industries (such as agriculture or manufacturing) and have seen the outmigration of talent and capital over the years.28 When a factory closes or crop prices fall, local wealth doesn’t have a cushion and can evaporate quickly, forcing families to deplete savings or go into debt. Additionally, assets common in rural areas (like small homes or used vehicles) do not appreciate in value as much as assets like urban real estate or stocks. All of this means that a child born in a low-wealth rural Georgia county faces an uphill climb to accumulate wealth in adulthood, even if their income improves.

It is precisely these disparities that baby bonds are designed to counteract. By seeding wealth for those who have very little or none at all, baby bonds could gradually even out the disparities and create a more balanced economic landscape in Georgia.

Asset Types Highlight Need for Broad Investment Tools for Georgians

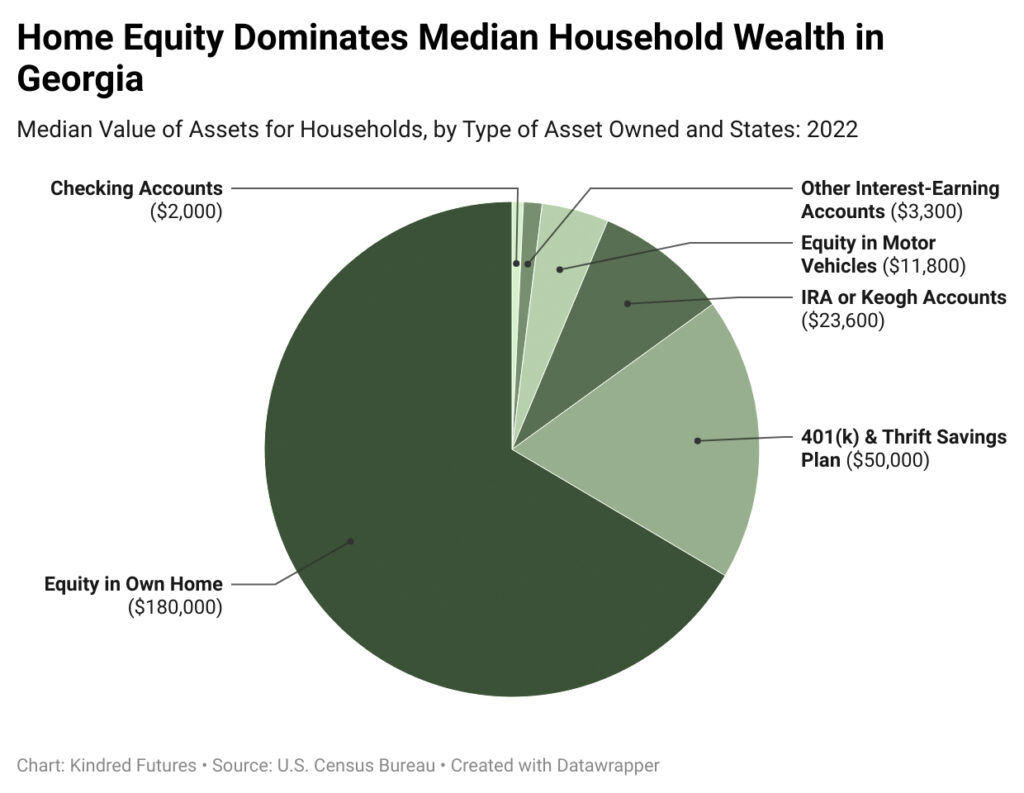

Home equity is the single largest component of household wealth in Georgia, exceeding even retirement savings and investment accounts. While it is expected to surpass lower-value assets like checking accounts or vehicles, the fact that it also outpaces higher-value, growth-oriented assets highlights how central homeownership is to wealth-building in the state. For families unable to afford a down payment or access credit, this creates a significant barrier to accumulating long-term wealth.29 The fact that the biggest share of median household wealth comes from owning a home underscore how critical an initial wealth starter can be.

Families from low-wealth backgrounds face multiple barriers to building home equity. First, many cannot afford the upfront costs of homeownership—especially the down payment—because they lack savings or family wealth transfers. This prevents them from accessing the primary pathway to long-term wealth accumulation in Georgia. Second, even those who do purchase homes often do so with smaller down payments, resulting in slower equity growth and greater vulnerability to market fluctuations. These structural disadvantages compound over time, making it harder to catch up with peers who entered the housing market with more capital, like retirement accounts or investment accounts.

There are also notable differences in how White and Black households in Georgia allocate their wealth across various asset categories. For White households, retirement accounts and primary residences each represent over a quarter of total holdings, with smaller yet meaningful shares in businesses, stocks, and mutual funds. In contrast, Black households direct nearly half of their asset portfolio toward business ownership, while retirement accounts and stocks make up relatively smaller proportions.30 This contrast points to distinct paths of wealth-building between the two groups, with White families more heavily invested in employer-sponsored or market-based vehicles (like 401(k)s and mutual funds), whereas Black families appear to rely more on entrepreneurial ventures and real estate for asset growth.

Households with a higher reliance on business ownership or real estate, for example, may face greater risks if they lack startup capital or resources to buffer against market swings.31 The variation in asset-holdings and values underscores why a universal policy that builds assets early on—rather than relying solely on traditional savings mechanisms—could be especially powerful in leveling the playing field for families who otherwise struggle to access stable, growth-oriented investments.