Georgia is poised to be a leader

in state-level Baby Bonds policy

Building on proposed legislation (2025 House Bill 284 and HR 99, 202547 ), this section outlines how a Georgia Baby Bonds program could work, compares design options, and evaluates their costs and benefits. The overarching goal is to maximize the program’s impact on narrowing the racial wealth gap and uplifting low-wealth communities, while ensuring financial and political feasibility.

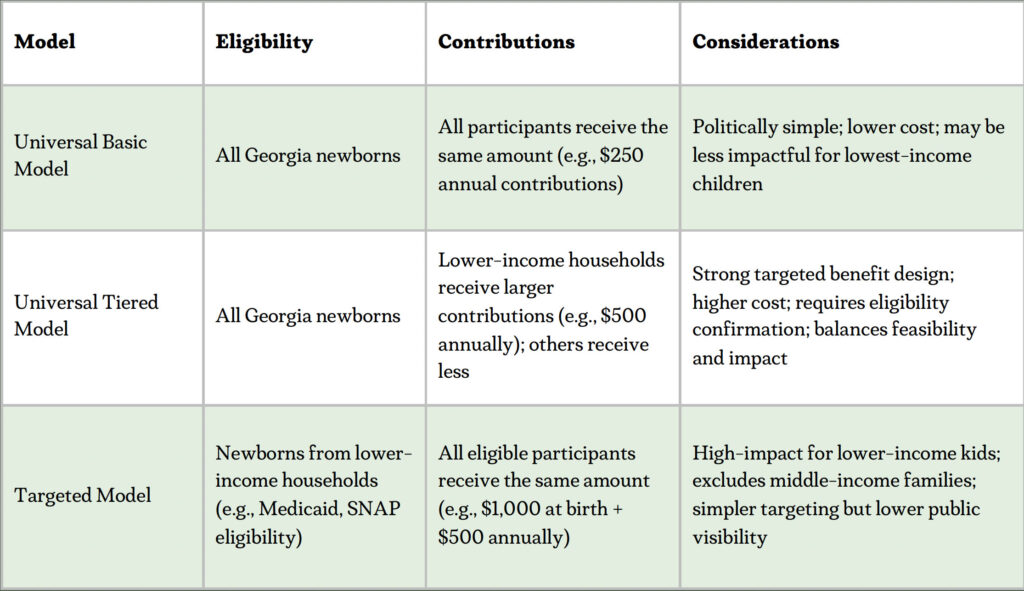

The core of baby bonds is simple: the state would deposit a sum of money into a trust fund for each eligible newborn, invest those funds until the child reaches adulthood, then allow the young adult to withdraw the money for approved uses. Within this policy, however, there are key design choices. Options range from a one-time deposit at birth to ongoing contributions throughout childhood. This report compares three models:

In evaluating the available baby bonds models for Georgia, we recommend a hybrid approach that combines universal eligibility with income-based tiered contributions, as proposed in GA House Bill 284.

This design achieves multiple policy objectives: it ensures near-universal participation, simplifies enrollment through automatic birth registration, and allocates greater resources to children most likely to face long-term asset deprivation. Georgia’s demographic and economic context justifies this approach. A majority of rural births are Medicaid-covered, indicating disproportionate exposure to intergenerational wealth constraints. A flat universal model may be administratively efficient but lacks the targeting necessary to meaningfully reduce disparities. Conversely, a strictly targeted model could undermine public buy-in and limit political feasibility by excluding moderate-income families who also lack asset-building tools.

By contrast, a universal tiered model maximizes efficiency. It directs higher-value contributions to the bottom of the wealth distribution, where public dollars have the greatest marginal impact, while maintaining broad political appeal through universal access. This approach aligns with research indicating that targeted asset investments in early life yield high long-term returns in education, employment, and tax contributions, and reduces downstream public costs related to housing instability, underemployment, and debt.

Designing an effective baby bonds program for Georgia requires careful attention to core implementation principles that ensure access, growth, and long-term impact. Below are five key principles that should guide program development:

-

Automatic Enrollment & Universal Access. Every child born in Georgia should be automatically enrolled in the baby bonds program at birth, ensuring that all eligible children—regardless of parental income, financial education, or bureaucratic barriers—receive a starting asset. By making the program universal and automatic, Georgia eliminates disparities in access and ensures that every child has a foundation for wealth-building.

-

Publicly Managed Trust with Guaranteed Growth. The state should invest baby bond funds in a public trust, managed to achieve stable, long-term growth with a minimum guaranteed return (e.g., 3-5 percent annually). Using a diversified investment strategy—similar to pension funds or sovereign wealth funds—the program ensures that each account grows over time. This structure allows the state to maximize wealth-building opportunities while maintaining responsible oversight and financial sustainability.

-

Guided Use with Flexible Guardrails at Withdrawal Age. Upon reaching eligibility at age 18 or higher, recipients should have broad flexibility in how they use their funds for wealth-building purposes such as education, homeownership, entrepreneurship, or relocation for employment. To balance agency with public accountability, the program could offer financial advising or planning resources to help participants make informed decisions and maximize long-term impact. These light-touch guardrails would build confidence in the program while preserving recipients’ ability to shape their economic futures.

-

Tiered Contribution Model for Targeted Impact. To address Georgia’s racial and rural-urban wealth divide, the program should use a tiered funding structure, providing larger contributions to children from lower-income households. While all children would receive a base deposit, additional contributions would be scaled by family income, ensuring that those with fewer financial resources receive the most significant support.

-

Statewide Wealth-Building & Economic Development Integration. Baby bonds should be integrated into Georgia’s broader strategy for inclusive economic growth. This includes aligning the program with existing wealth-building policies—such as first-time homebuyer incentives, small business capital access, and rural revitalization efforts and leveraging partnerships to provide financial education and outreach in disinvested communities.

A scalable baby bonds policy with automatic enrollment and tiered contributions would support a modest yet high-return investment in the next generation’s economic future.

Notably, there are ways to mitigate the budgetary impact for the state: for example, establishing an endowment or trust fund today that grows and pays out benefits 18 years later, or using state bond financing (spread over decades) to fund the accounts upfront. The return on investment (ROI) for Georgia’s economy could be substantial. If tens of thousands of young Georgians each year enter adulthood with assets, we can expect higher college completion rates, greater entrepreneurship, and increased homeownership. Under House Bill 284, Georgia’s youth and young adults can acquire an estimated $1.4 billion in wealth per birth cohort to invest in Georgia’s economy when they reach the age of 18.48

The map illustrates the projected per capita wealth gains for newborns in Georgia under House Bill 284, showing how Baby Bonds have the greatest relative impact in rural counties. While absolute wealth accumulation is higher in Metro Atlanta due to larger populations, this per capita analysis highlights where each child stands to benefit the most. The darker-shaded counties, concentrated in South and Central Georgia, reflect areas where a higher proportion of newborns qualify for the larger $15,000 baby bonds contribution, leading to greater wealth-building potential. In contrast, lighter-shaded counties, primarily in affluent suburban and metro areas, have lower per-child wealth gains due to a smaller share of low-income births. This visualization reinforces how baby bonds can help close wealth disparities between rural and urban communities, ensuring that children born in Georgia’s lowest-income counties have: stronger financial foundation by adulthood.

Under House Bill 284, Georgia’s youth and young adults can acquire an estimated $1.4 billion in wealth per birth cohort to invest in Georgia’s economy when they reach the age of 18.