References

1 Allums, C. A., Markley, S. N., & Hafley, T. J. (2022). “A better place to be”? Black Mecca, White democracy, and the contradictions of neoliberal cityhood in Atlanta’s Black suburbs. Journal of Urban Affairs, 44(6), 793-807.

2 Jackson, Dylan. “Atlanta Has the Highest Income Inequality in the Nation, Census Data Shows.” The Atlanta Journal-Constitution, Nov 28, 2022, sec. Investigations.

3 Price, Anne. “Don’t Fixate on the Racial Wealth Gap: Focus on Undoing Its Root Causes.” Insight Center (blog), February 5, 2020. https://insightcced.org/dont-fixate-on-the-racial-wealth-gap-focus-on-undoing-its-root-causes/.

4 AWBI analysis of American Community Survey data, 2017-2021 5-year estimates

5 AWBI analysis of “Financial Health and Wealth Dashboard.” Urban Institute, October 6, 2022. https://urbn.is/ 3DKam1u.

6 Ibid.

7 Asante-Muhammad, Dedrick, Chuck Collins, Josh Hoxie, and Emanuel Nieves. “The Road to Zero Wealth: How the Racial Wealth Divide Is Hollowing out America’s Middle Class.” Report. Prosperity Now, Institute for Policy Studies, September 1, 2017. United States of America. https://apo.org.au/node/220721.

8 A. Darity, William, and Kirsten A. Mullen. From Here to Equality, Second Edition: Reparations for Black Americans in the Twenty-First Century. UNC Press Books, 2022.

9 “War in Our Backyards.” Accessed October 6, 2023. https://battleofatlanta.ajc.com/part1.html.

10 Atlanta History Center. “A City Enslaved | The Color-Line: The Problem of the Centuries | Exhibitions.” Accessed October 6, 2023. https://www.atlantahistorycenter.com/exhibitions/the-color-line-the-problem-of-the-centuries/a- city-enslaved/.

11 Camardelle, Alex. “Telling the Unvarnished Truth About Georgia.” Georgia Budget and Policy Institute (blog), February 26, 2020. https://gbpi.org/telling-the-unvarnished-truth-about-georgia/.

12 Godshalk, David Fort. Veiled visions: The 1906 Atlanta race riot and the reshaping of American race relations. Univ of North Carolina Press, 2006.

13 Hobson, Maurice J. The legend of the Black mecca: Politics and class in the making of modern Atlanta. UNC Press Books, 2017.

14 Ibid.

15 Williams, Janelle, and Sarah Torian. “Changing the Odds.” The Annie E. Casey Foundation, June 24, 2015. https://www.aecf.org/resources/changing-the-odds.

16 Toone, Stephanie. “Forbes: These Are the Top Cities Where African-Americans Are Doing the Best Economically.” The Atlanta Journal-Constitution, January 2020. https://www.ajc.com/news/the-cities-where-african- americans-are-doing-the-best

17 Frey, William. “A 2020 Census Portrait of America’s Largest Metro Areas: Population growth, diversity, segregation, and youth.” (2022): 1.

18 “Advancing Collective Prosperity through Entrepreneurship in Atlanta | Prosperity Now,” January 23, 2018. https://prosperitynow.org/resources/advancing-collective-prosperity-through-entrepreneurship-atlanta.

19 AWBI analysis of American Community Survey data, U.S. Census Bureau

20 AWBI analysis of “Prosperity Now Scorecard.” Prosperity Now, October 6, 2023.

21 Ibid.

22 AWBI analysis of “Metro Atlanta Speaks survey.” Atlanta Regional Commission, October 6, 2023. https:// 33n.atlantaregional.com/mas

23 AWBI analysis of American Community Survey data, U.S. Census Bureau

24 Ibid.

25 Thompson, Jeffrey P., and Gustavo Suarez. “Accounting for racial wealth disparities in the United States.” (2019).

26 Aladangady, Aditya, and Akila Forde. “Wealth Inequality and the Racial Wealth Gap,” October 22, 2021. https:// www.federalreserve.gov/econres/notes/feds-notes/wealth-inequality-and-the-racial-wealth-gap-20211022.html.

27 Leonhardt, David. “In Climbing Income Ladder, Location Matters.” The New York Times, July 22, 2013, sec. U.S. https://www.nytimes.com/2013/07/22/business/in-climbing-income-ladder-location-matters.html.

28 AWBI analysis of American Community Survey data, US Census Bureau

29 Brookings. “Long Shadows: The Black-White Gap in Multigenerational Poverty.” Accessed October 6, 2023. https://www.brookings.edu/articles/long-shadows-the-black-white-gap-in-multigenerational-poverty/.

30 Sullivan, Laura, Tatjana Meschede, Lars Dietrich, and Thomas Shapiro. “The racial wealth gap.” Institue for Assests and Social Policy, Brandeis University. Demos (2015).

31 Hicks, Natasha, Fenaba Addo, Anne Price, and William Darity Jr. “Still Running Up the Down Escalator: How Narratives Shape our Understanding of Racial Wealth Inequality.” Samuel DuBois Cook Center on Social Equity (2021).

32 AWBI analysis of American Community Survey data, U.S. Census Bureau

33 AWBI analysis of American Community Survey data, U.S. Census Bureau

34 Aliprantis, Dionissi, and Daniel R. Carroll. “What is behind the persistence of the racial wealth gap?.” Economic Commentary 2019-03 (2019).

35 Demos. “The Racial Wealth Gap: Why Policy Matters.” Accessed October 27, 2023. https://www.demos.org/research/racial-wealth-gap-why-policy-matters.

36 Hicks, Natasha, Fenaba Addo, Anne Price, and William Darity Jr. “Still Running Up the Down Escalator: How Narratives Shape our Understanding of Racial Wealth Inequality.” Samuel DuBois Cook Center on Social Equity (2021).

37 Ibid.

38 Wright, Will. “Atlanta Migration Patterns: A Closer Look (Pt. 2).” 33n (blog), February 2, 2023. https:// 33n.atlantaregional.com/regional-snapshot/atlanta-migration-patterns-a-closer-look-pt-2.

39 AWBI analysis of American Community Survey data, U.S. Census Bureau

40 Hamil-Luker, Jenifer, and Angela M. O’Rand. “Black/White Differences in the Relationship between Debt and Risk of Heart Attack across Cohorts.” SSM – Population Health 22 (February 25, 2023): 101373. https://doi.org/ 10.1016/j.ssmph.2023.101373.

41 Stewart III, Shelley et al. “The Economic State of Black America: What Is and What Could Be | McKinsey.” Accessed October 6, 2023. https://www.mckinsey.com/featured-insights/diversity-and-inclusion/the-economic-state- of-Black-america-what-is-and-what-could-be#/.

42 AWBI analysis of “Financial Health and Wealth Dashboard.” Urban Institute, October 6, 2022. https://urbn.is/ 3DKam1u.

43 “The Complex Story of American Debt,” July 29, 2015. http://bit.ly/1DJ4xbL.

44 AWBI analysis of “Financial Health and Wealth Dashboard.” Urban Institute. October 6, 2023.

45 Berliner, Benjamin. “The Burden of Debt on Mental and Physical Health.” The Aspen Institute, August 2, 2018. https://www.aspeninstitute.org/blog-posts/hidden-costs-of-consumer-debt/.

46 Hamil-Luker, Jenifer, and M. O. Angela. “Black/white differences in the relationship between debt and risk of heart attack across cohorts.” SSM-population health 22 (2023): 101373.

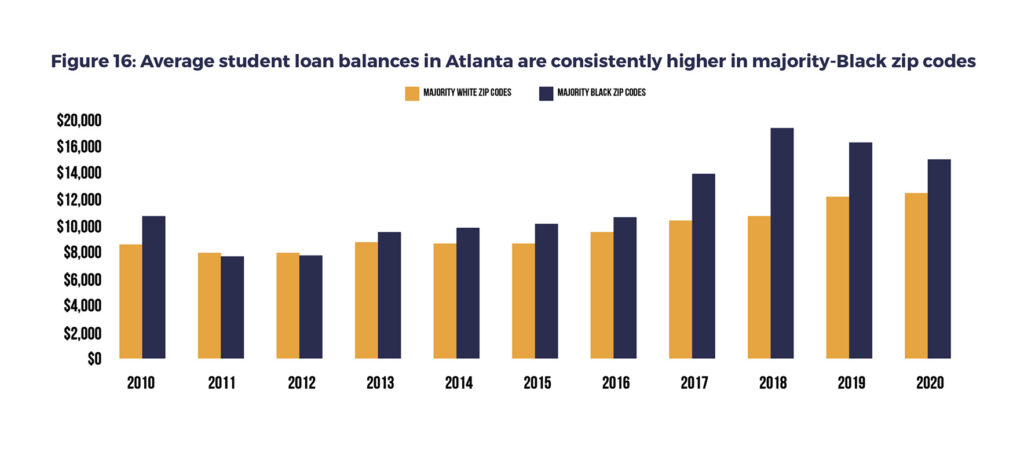

47 Jackson, Victoria, and Jalil B. Mustaffa. “Student Debt Is Harming the Mental Health of Black Borrowers.” Education Trust (2022).

48 Center, Student Borrower Protection. “The South Has Something to Say: Atlanta.” Student Borrower Protection Center Research Paper (2023).

49 Ibid.

50 McNamara –, John. “Debt Collectors Re-Evaluate Medical Debt Furnishing in Light of Data Integrity Issues.”Consumer Financial Protection Bureau, February 14, 2023. https://www.consumerfinance.gov/about-us/blog/debt- collectors-re-evaluate-medical-debt-furnishing-in-light-of-data-integrity-issues/.

51 AWBI analysis of “Financial Health and Wealth Dashboard.” Urban Institute. October 6, 2023.

52 A Survey of Georgia Residents: State of the State”. The Southern Economic Advancement Project. June, 2022

53 Wiltshire, Jacqueline C., Keith Elder, Catarina Kiefe, and Jeroan J. Allison. “Medical Debt and Related Financial Consequences Among Older African American and White Adults.” American Journal of Public Health 106, no. 6 (June 2016): 1086–91. https://doi.org/10.2105/AJPH.2016.303137.

54 AWBI analysis of American Community Survey data

55 AWBI analysis of “Financial Health and Wealth Dashboard.” Urban Institute. October 6, 2023.

56 Ruetschlin, Catherine, and Dedrick Asante-Muhammad. “The challenge of credit card debt for the African American middle class.” (2013).

57 U.S. Census Bureau. “COVID-19 Pandemic Hit Black Households Harder Than White Households, Even When Pre-Pandemic Socio-Economic Disparities Are Taken Into Account.” Census.gov. Accessed October 6, 2023. https:// www.census.gov/library/stories/2021/07/how-pandemic-affected-black-and-white-households.html.

58 Rice, Lisa, and Deidre Swesnik. “Discriminatory effects of credit scoring on communities of color.” Suffolk UL Rev. 46 (2013): 935.

59 Ratcliffe, Caroline, and Steven Brown. “Credit scores perpetuate racial disparities, even in America’s most prosperous cities.” Urban Wire-the Blog of the Urban Institute (2017).

60 Ibid.

61 Brevoort, Kenneth P., Jasper Clarkberg, Michelle Kambara, and Benjamin Litwin. “The geography of credit invisibility.” Consumer Financial Protection Bureau Office of Research Reports Series 18-6 (2018).

62 Ibid.

63 Todd, Tim, and Esther L. George. Let Us Put Our Money Together: The Founding of America’s First Black Banks. Public Affairs Department of the Federal Reserve Bank of Kansas City, 2019.

64 Ibid.

65 Ibid. pp. 106

66 Lewis, Willard. “Citizens Trust Bank.” New Georgia Encyclopedia, lab modified Od 30, 2021. heps:// www.georgiaencyclopedia.org/arVcles/business-economy/ciVzens-trub-bank/

67 Toussaint-Comeau, Maude, and Robin Newberger. “Minority-owned banks and their primary local market areas.” Economic Perspectives 4, no. 4 (2017): 1-31.

68 AWBI analysis of “FDIC lists of Minority Depository Institutions (MDIs) Second Quarter 2023.” FDIC. October 20, 2023

69 Mattos, Trevor, and Matthew Brewster. “The Color of the Capital Gap.” Boston Indicators, 2021. https:// www.bostonindicators.org/reports/report-detail-pages/color-of-the-capital-gap.

70 Ibid.

71 Board of Governors of the Federal Reserve System. “The Community Reinvestment Act.” Accessed October 7, 2023. https://www.federalreserve.gov/newsevents/testimony/braunstein20080213a.htm.

72 Blower, Brad, Josh Silver, Jason Richardson, Glenn Schlactus, and Sacha Markano-Stark. “Adding Robust Consideration of Race to Community Reinvestment Act Regulations: An Essential and Constitutional Proposal – NCRC.” National Community Reinvestment Coalition, 2021. https://ncrc.org/adding-robust-consideration-of-race- to-community-reinvestment-act-regulations-an-essential-and-constitutional-proposal/.

73 Haspel, Moshe. “The Decline of Bank Branches and the Rise of Atlanta Banking Deserts.” 33n (blog), September 8, 2023. https://33n.atlantaregional.com/data-diversions/the-decline-of-bank-branches-and-the-rise-of-atlanta- banking-deserts.

74 “CDFI Certification | Community Development Financial Institutions Fund.” Accessed Odober 13, 2023. heps:// www.cdfifund.gov/programs-training/cerVficaVon/cdfi.

75 Fund, Reinvebment. “A Conversaton with Georgia’s Community Development Financial Institutions (CDFI): CDFIs Are Quietly Multiplying in Georgia, Creating a Wealth of Opportunity.” SaportaReport, Odober 13, 2022. hep:// saportareport.com/a-conversation-with-georgias-community-development-financial-institutions-cdfi-cdfis-are- quietly-multiplying-in-georgia-creating-a-wealth-of-opportunity/thought-leadership/reinvestment-fund/.

76 AWBI analysis of “Prosperity Now Scorecard.” Prosperity Now. October 7, 2023

77 Bot Populi. “How Fintech Became the Gateway to Predatory Lending in Sub-Saharan Africa.” Accessed October 7, 2023. https://botpopuli.net/?post_type=post&p=7278.

78 AWBI analysis of data from the FDIC National Survey of Unbanked and Underbanked Households

79 Darity Jr, William, Darrick Hamilton, Mark Paul, Alan Aja, Anne Price, Antonio Moore, and Caterina Chiopris.“What we get wrong about closing the racial wealth gap.” Samuel DuBois Cook Center on Social Equity and Insight Center for Community Economic Development 1, no. 1 (2018): 1-67.

80 Holloway, Steven R., and Elvin K. Wyly. “” The Color of Money” Expanded: Geographically Contingent Mortgage Lending in Atlanta.” Journal of Housing Research (2001): 55-90.

81 Dreier, Peter. “Redlining cities: How banks color community development.” Challenge 34, no. 6 (1991): 15-23.

82 Holloway, Steven R., and Elvin K. Wyly. “” The Color of Money” Expanded: Geographically Contingent Mortgage Lending in Atlanta.” Journal of Housing Research (2001): 55-90.

83 U.S. Department of Housing and Urban Development (HUD). “History of Fair Housing – HUD.” Accessed October 7, 2023. https://www.hud.gov/program_offices/fair_housing_equal_opp/aboutfheo/history.

84 Ibid.

85 “Civil Rights Division | Housing And Civil Enforcement Cases Documents,” August 6, 2015. https:// www.justice.gov/crt/housing-and-civil-enforcement-cases-documents-485.

86 “More Americans Own Their Homes, but Black-White Homeownership Rate Gap Is Biggest in a Decade, NAR Report Finds,” March 2, 2023. https://www.nar.realtor/newsroom/more-americans-own-their-homes-but-black- white-homeownership-rate-gap-is-biggest-in-a-decade-nar.

87 Rothwell, Johnathan, and Andre Perry. “How Racial Bias in Appraisals Affects the Devaluation of Homes in Majority-Black Neighborhoods.” Brookings. Accessed October 12, 2023. https://www.brookings.edu/articles/how-racial-bias-in-appraisals-affects-the-devaluation-of-homes-in-majority-black-neighborhoods/.

88 Home Mortgage Disclosure Act (HMDA) data, accessed via DataNexus

89 Tracking Homeownership Wealth Gaps.” Accessed October 13, 2023. https://urbn.is/2YQ33Dz.

90 Perry, Andre. “The devaluation of assets in black neighborhoods: How racism robs homeowner of the American Dream.” (2019).

91 Ibid.

92 Du Bois, William Edward Burghardt, ed. The Negro in business: report of a social study made under the direction of Atlanta University, together with the proceedings of the fourth Conference for the Study of the Negro Problems, held at Atlanta University, May 30-31, 1899. No. 4. Atlanta University, 1899.

93 Atlanta History Center. “Sweet Auburn | Atlanta in 50 Objects | Exhibitions.” Accessed October 7, 2023. https:// www.atlantahistorycenter.com/exhibitions/atlanta-in-50-objects/sweet-auburn/.

94 Ibid.

95 Youngblood, Mtamanika. “The Historic District Development Corporation and the Challenge of Urban Revitalization.” In Planning Atlanta, pp. 40-48. Routledge, 2017.

96 Bates, Timothy. “CONTESTED TERRAIN: The Role of Preferential Policies in Opening Government and Corporate Procurement Markets to Blaq-Owned Businesses.” Du Bois Review: Social Science Research on Race 12, no. 1 (2015): 137–59. doi:10.1017/S1742058X14000289.

97 Levy, Jessica Ann. “Selling Atlanta: Black Mayoral Politics from Protest to Entrepreneurism, 1973 to 1990.” Journal of Urban History 41, no. 3 (May 2015): 420–43. https://doi.org/10.1177/0096144214566953.

98 City of Atlanta, City Auditor’s Office. “Office of Contract Compliance – June 2021.” Accessed October 12, 2023. http://www.atlaudit.org/office-of-contract-compliance—june-2021.html.

99 AWBI analysis of Annual Business Survey data, U.S. Census Bureau

100 Meyer, Bruce D. “Why are there so few black entrepreneurs?.” (1990).

101 Wiersch., Ann Marie, and Lucas Misera. “2022 Report on Firms Owned by People of Color Based on the Small Business Credit Survey.” Small Business Credit Survey Federal Reserve Banks, no. 20220629 (June 29, 2022). heps://doi.org/10.55350/sbcs-20220629.

102 Corcoran, Emily Wavering, Jordan Manes, Lucas Misera, and Ann Marie Wiersch. “2023 Report on Employer Firms: Findings from the 2022 Small Business Credit Survey.” Small Business Credit Survey Publications, no. 20220308 (March 8, 2022). https://doi.org/10.55350/sbcs-20230308.

103 Lincoln Quillian, Devah Pager, Ole Hexel, and Arnfinn H. Midtbøen, “Meta-analysis of Field Experiments Shows No Change in Racial Discrimination in Hiring Over Time,” Proceedings of the National Academy of Sciences 114 (41) (2017): 10870-875.

104 Devah Pager, Bruce Western, and Naomi Sugie, “Sequencing Disadvantage: Barriers to Employment Facing Young Black and White Men with Criminal Records,” The Annals of the American Academy of Political and Social Science 623 (1) (2009): 195-213.

105 Maryam Jameel and Joe Yerardi, “Workplace Discrimination is Illegal. But Our Data Shows it’s Still a Huge Problem,” Vox, February, 2019.

106 Hicks, Natasha, Fenaba Addo, Anne Price, and William Darity Jr. “Still Running Up the Down Escalator: How Narratives Shape our Understanding of Racial Wealth Inequality.” Samuel DuBois Cook Center on Social Equity (2021).

107 Torian, S., West, A., & Williams, J. (2019). Changing the Odds: Progress and Promise in Atlanta. Annie E. Casey Foundation.

108 AWBI Analysis of American Community Survey data, U.S. Census Bureau

109 Schneider, Daniel, and Kristin Turney. “Incarceration and black–white inequality in homeownership: A state- level analysis.” Social Science Research 53 (2015): 403-414.

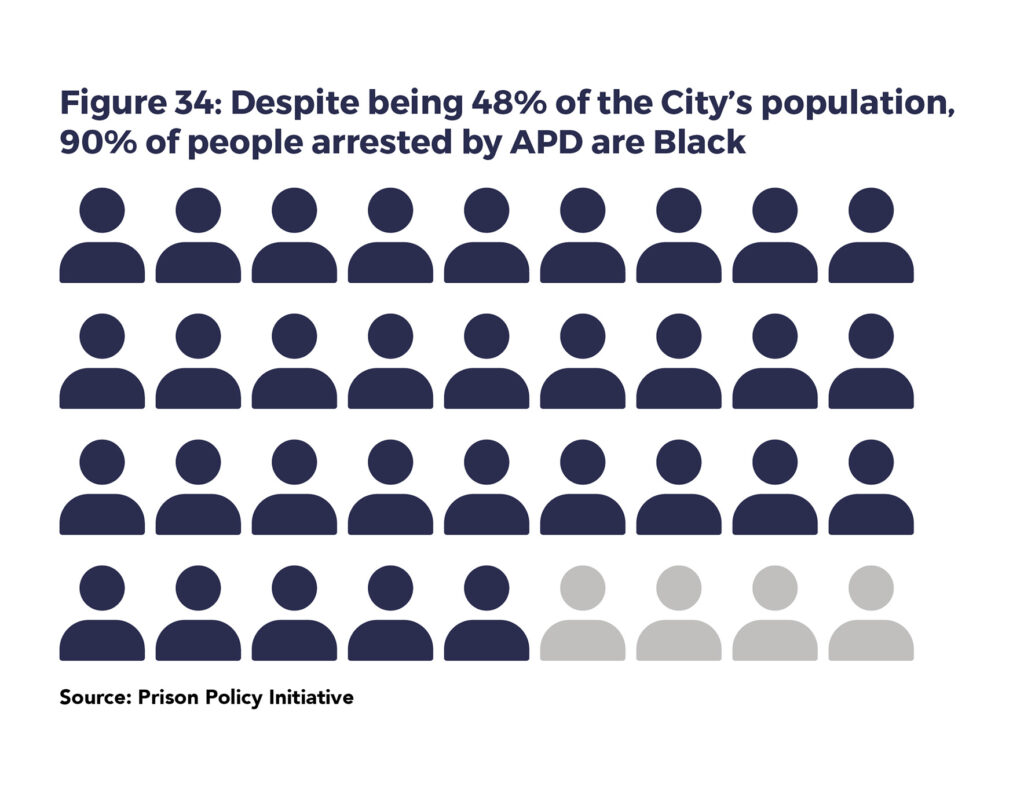

110 “Mass Incarceration.” Atlanta, Georgia: Southern Center for Human Rights, 2023. https://www.schr.org/mass-incarceration/#:~:text=With%20one%20out%20of%20every,second%2Dhighest%20correctional%20control%20rate.

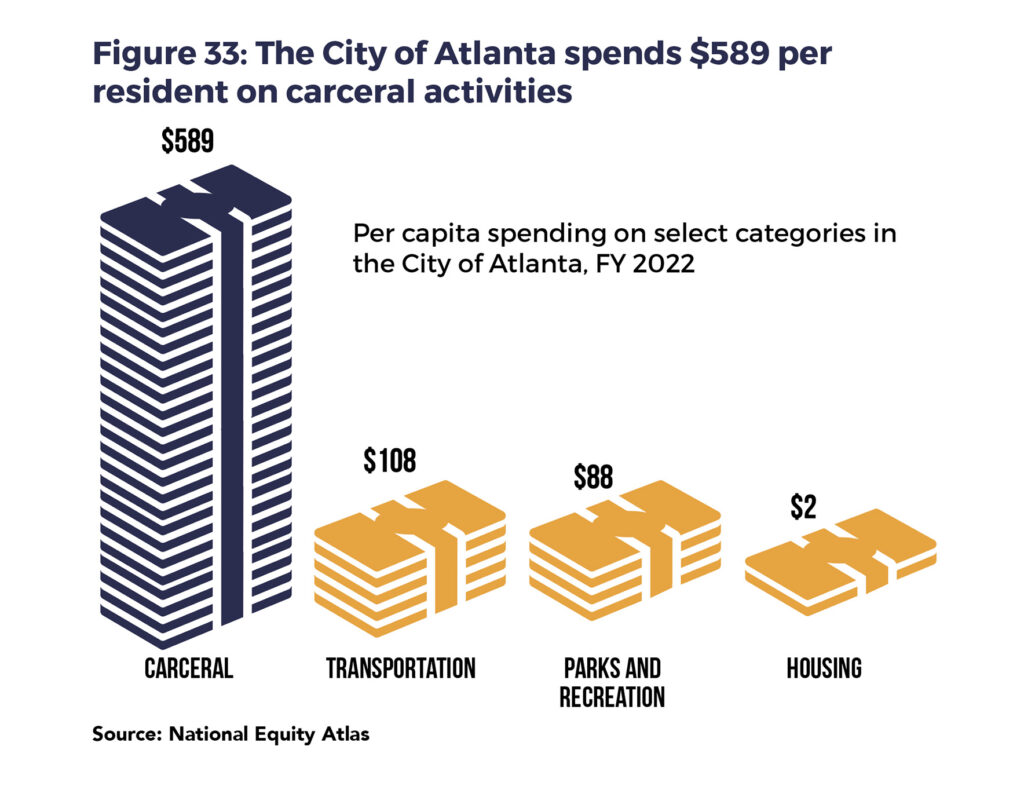

111 National Equity Atlas. At What Cost? Examining Police, Sheriff, and Jail Budgets Across the US (dashboard). Accessed at: https://nationalequityatlas.org/us-carceral-spending/dashboard

112 Booker, Meredith. “The wealth of incarcerated versus non-incarcerated men over a lifetime, visualized”. Prison Policy Initiative (2016). Accessed at: https://www.prisonpolicy.org/blog/2016/04/26/wealth/#:~:text=Previous%20research%20in%20Black%20Wealth,men%20who%20never%20experienced%20incarceration.

113 Zaw, Khaing, Darrick Hamilton, and William Darity. “Race, wealth and incarceration: Results from the National Longitudinal Survey of Youth.” Race and Social Problems 8 (2016): 103-115.

114 Maroto, Michelle, and Bryan L. Sykes. “The varying effects of incarceration, conviction, and arrest on wealth outcomes among young adults.” Social Problems 67, no. 4 (2020): 698-718.

115 Policing Alternatives & Diversion Initiative. “Jail Population Review Committee.” Accessed October 26, 2023. https://www.atlantapad.org/jail-population-review.

116 Atlanta History Center. “Students and Strategy | The Color-Line: The Problem of the Centuries | Exhibitions.”Accessed October 7, 2023. https://www.atlantahistorycenter.com/exhibitions/the-color-line-the-problem-of-the- centuries/students-and-strategy/.

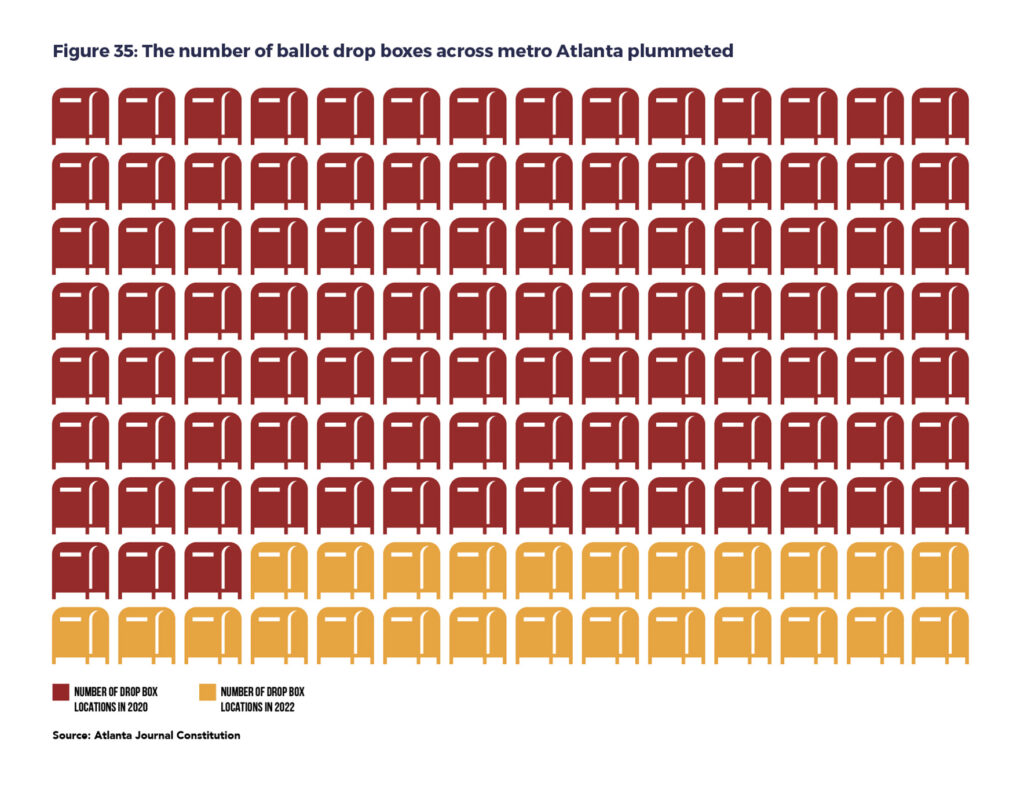

117 Collins, Keith, Ford Fessenden, Lazaro Gamio, Rich Harris, John Keefe, Denise Lu, Eleanor Lutz, AmySchoenfeld Walker, Derek Watkins, and Karen Yourish. “Tight Georgia Race Comes Down to Metro Atlanta.” The New York Times, November 4, 2020, sec. U.S. https://www.nytimes.com/interactive/2020/11/04/us/elections/ georgia-election-results-atlanta.html.

118 Fowler, Stephen, Sam Gringlas, and Huo Jingnan. “A New Georgia Voting Law Reduced Ballot Drop Box Access in Places That Used Them Most.” WABE, July 27, 2022. https://www.wabe.org/a-new-georgia-voting-law-reduced-ballot-drop-box-access-in-places-that-used-them-most/.

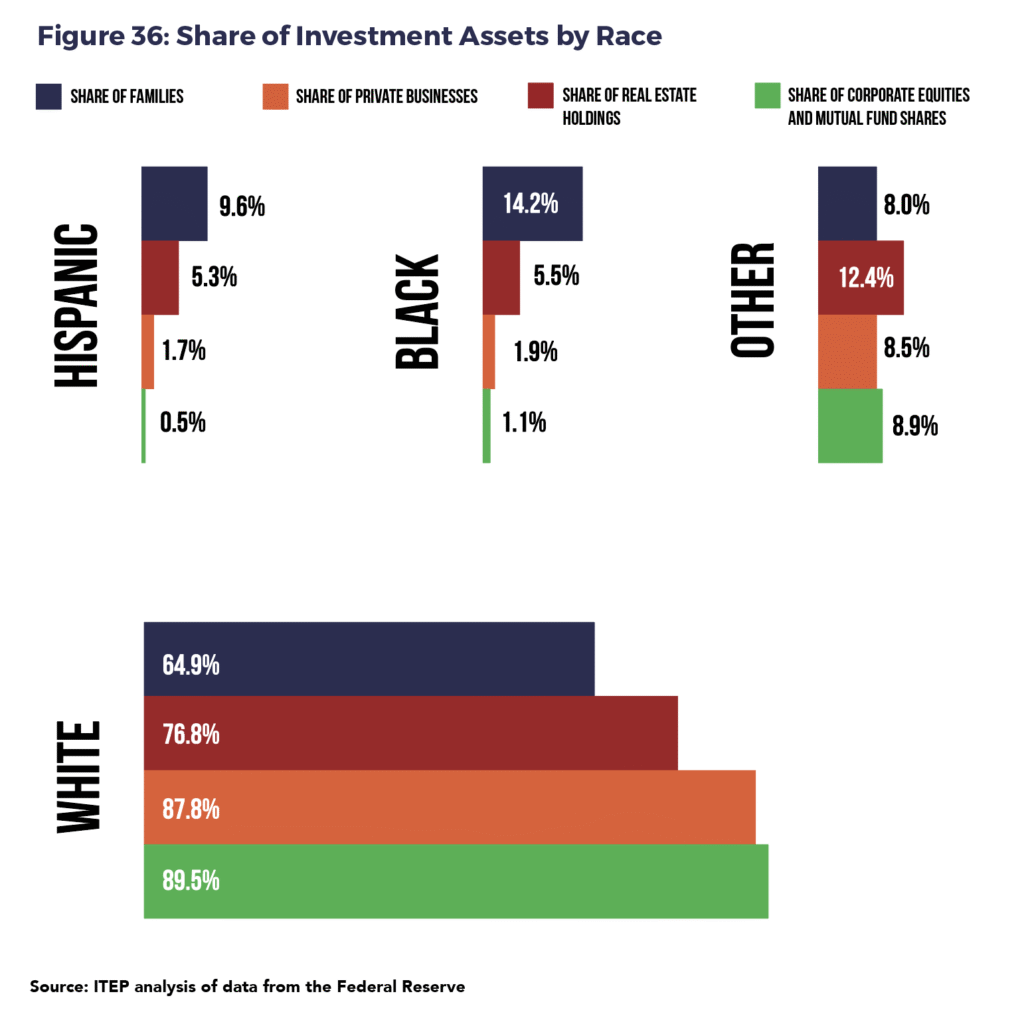

119 Derenoncourt, Ellora, Chi Hyun Kim, Moritz Kuhn, and Moritz Schularick. Wealth of two nations: The US racial wealth gap, 1860-2020. No. w30101. National Bureau of Economic Research, 2022.

120 ITEP. “Investment Income and Racial Inequality.” Accessed October 20, 2023. https://itep.org/investment-income-and-racial-inequality/.

121 Derenoncourt, Ellora, Chi Hyun Kim, Moritz Kuhn, and Moritz Schularick. Wealth of two nations: The US racial wealth gap, 1860-2020. No. w30101. National Bureau of Economic Research, 2022.

122 Love, Hanna, and Manann Donoghoe. “The Black-White Wealth Gap Left Black Households More Vulnerable.” Brookings. Accessed October 20, 2023. https://www.brookings.edu/articles/the-black-white-wealth-gap-left-black-households-more-vulnerable/.

123 Oliver, Melvin, L. and Thomas M. Shapiro (2006) Black Wealth/White Wealth, New York: Routledge, pp. 18-252; Brown, Dorothy (2021) The Whiteness of Wealth. New York: Penguin Random House.

124 ITEP. “Georgia: Who Pays? 6th Edition.” Accessed October 20, 2023. https://itep.org/georgia/.

125 Stokes, Stephanie. “Black Neighborhoods Bear the Brunt of Fulton’s Tax Auctions. What Could Change That?” WABE, May 8, 2023. https://www.wabe.org/black-neighborhoods-bear-the-brunt-of-fultons-tax-auctions-what-could-change-that/.

126 Ibid.

127 Howell, Junia, and James R. Elliott. “Damages done: The longitudinal impacts of natural hazards on wealth inequality in the United States.” Social problems 66, no. 3 (2019): 448-467.

128 “CDC/ATSDR Social Vulnerability Index (SVI) | Place and Health | ATSDR,” August 2, 2023. https://www.atsdr.cdc.gov/placeandhealth/svi/interactive_map.html.

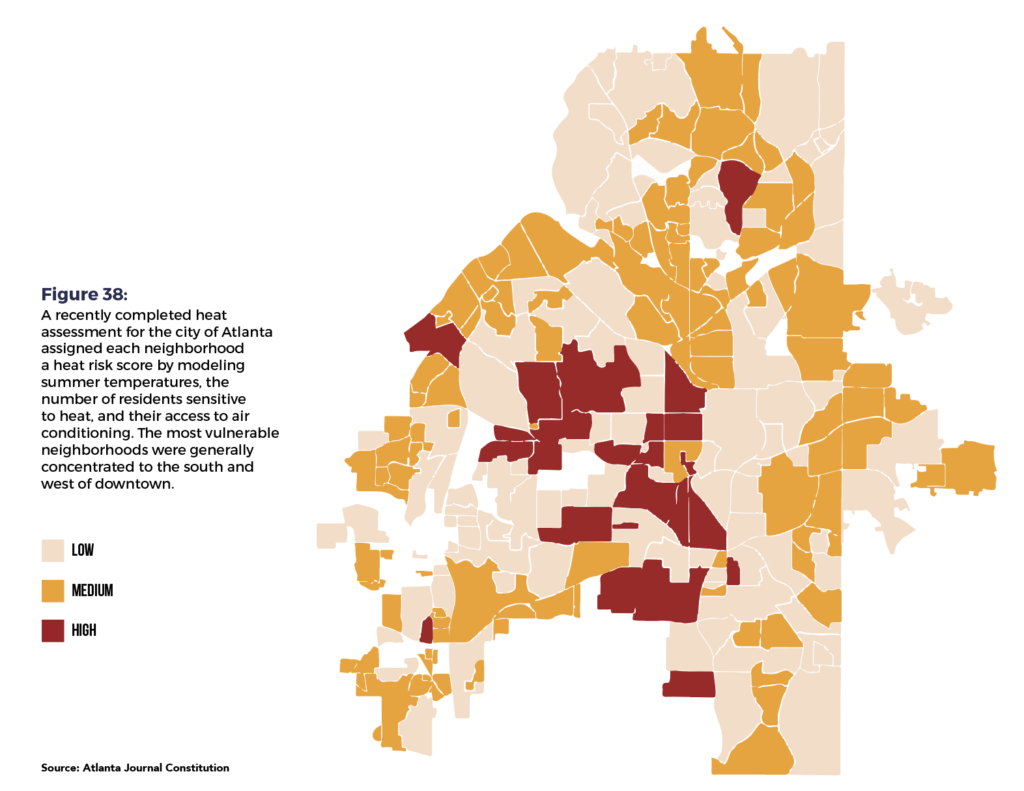

129 Kann, Drew, and Meris Lutz. “Heat Risk Is Growing. These Are Atlanta’s Most Vulnerable Neighborhoods.” The Atlanta Journal-Constitution, July 20, 2023, sec. Local News.

130 Data from GreenLink Analytics, GreenLink Equity Map (GEM) 2017

131 “Bank On Atlanta.” Accessed October 8, 2023. https://bankon.atlantaga.gov/.

132 Hudáková, V., Antonides, G., & Haagsma, R. (2015). The impact of a basic income on labor and work performance. Wageningen University of Life Sciences and Research Centre. Work Performance.

133 “Bank On Atlanta.” Accessed October 8, 2023. https://bankon.atlantaga.gov/.

134 WABE. “Georgia Bill to Require Bail for More Crimes Fails to Pass,” March 30, 2023. https://www.wabe.org/georgia-bill-to-require-bail-for-more-crimes-fails-to-pass/.

135 Blasi, Joseph, Douglas Kruse, and Dan Weltmann. “Guest editorial: New research on the impact of COVID-19 on employee-owned firms and the racial wealth gap in the context of the research literature.” Journal of Participation and Employee Ownership 4, no. 2 (2021): 89-91.

136 Boguslaw, J., & Schur, L. (2019). Building the Assets of Low and Moderate Income Workers and their Families.

137 Camardelle, Alex. “Women-Powered Prosperity.” Georgia Budget and Policy Institute (blog), September 10, 2019. https://gbpi.org/women-powered-prosperity-report/.

138 Economic Policy Institute, (2018). Worker rights preemption in the U.S.: A map of the campaign to suppress worker rights in the states. Accessed August 2019. https://www.epi.org/ preemption-map/

139 AWBI analysis of American Community Survey data, 2017-2021 five-year estimates

140 Brookings. “How Equity Isn’t Built into the Infrastructure Bill—and Ways to Fix It.” Accessed October 8, 2023. https://www.brookings.edu/articles/how-equity-isnt-built-into-the-infrastructure-bill-and-ways-to-fix-it/.

141 Darity Jr, William A., and A. Kirsten Mullen. From here to equality: Reparations for Black Americans in the twenty-first century. UNC Press Books, 2022.

142 Guarino, Mark. “Evanston, Ill., leads the country with first reparations program for Black residents.” Washington Post. https://www. washingtonpost. com/national/evanston-illinois-reparations/2021/03/22/6b5a308c-8b2d-11eb-9423-04079921c915_story. html (2021).

143 The King Center. “The King Philosophy – Nonviolence365®.” Accessed October 8, 2023. https://thekingcenter.org/about-tkc/the-king-philosophy/.